According to Gartner, the Buy Now, Pay Later (BNPL) market will grow to USD 911.8 billion in 2030. This shows the rising trends among both Gen Z and Millennials to use the flexible payment option like BNPL. The BNPL market will grow to USD 286.02 billion by 2034 at 23% CAGR. The cost of BNPL app development is likely to remain within USD 30,000 to USD 40,000.

Considering this, many businesses, especially FinTech and eCommerce app development companies. Many startups and businesses in the BFSI industry also want to build BNPL apps to meet the rising demand for the BNPL payment option.

Whether you are a business owner who wants to give your consumers a BNPL option or a FinTech startup that wants to incorporate this feature, the question looms: What is the cost to build a BNPL app?.

Well, it’s the right question that comes to mind when anyone wants to build this app. Without having the correct approach and the business goal to accomplish, it is not easy to get the cost estimation.

This blog on BNPL app development cost helps a business get the correct information about the cost of building a BNPL app. We also look at the factors that play a vital role in assessing the cost of BNPL app development.

What is a BNPL App?

Before looking at the BNPL app development cost, let’s know about it first, so we will all understand the same and remain on the same page.

A BNPL app enables the users of a business to purchase a product or service and pay for it later. The payment mode is through easy EMIs (with or without interest) instead of giving it upfront.

Let’s understand this with a simple example.

A girl is shopping online through a mobile app and has found the desired product.

However, the product’s cost is more than her budget. So, she chose the Buy Now, Pay Later option.

Over the next few weeks, the girl paid the amount with easy EMIs.

Read More: Best BNPL shopping apps

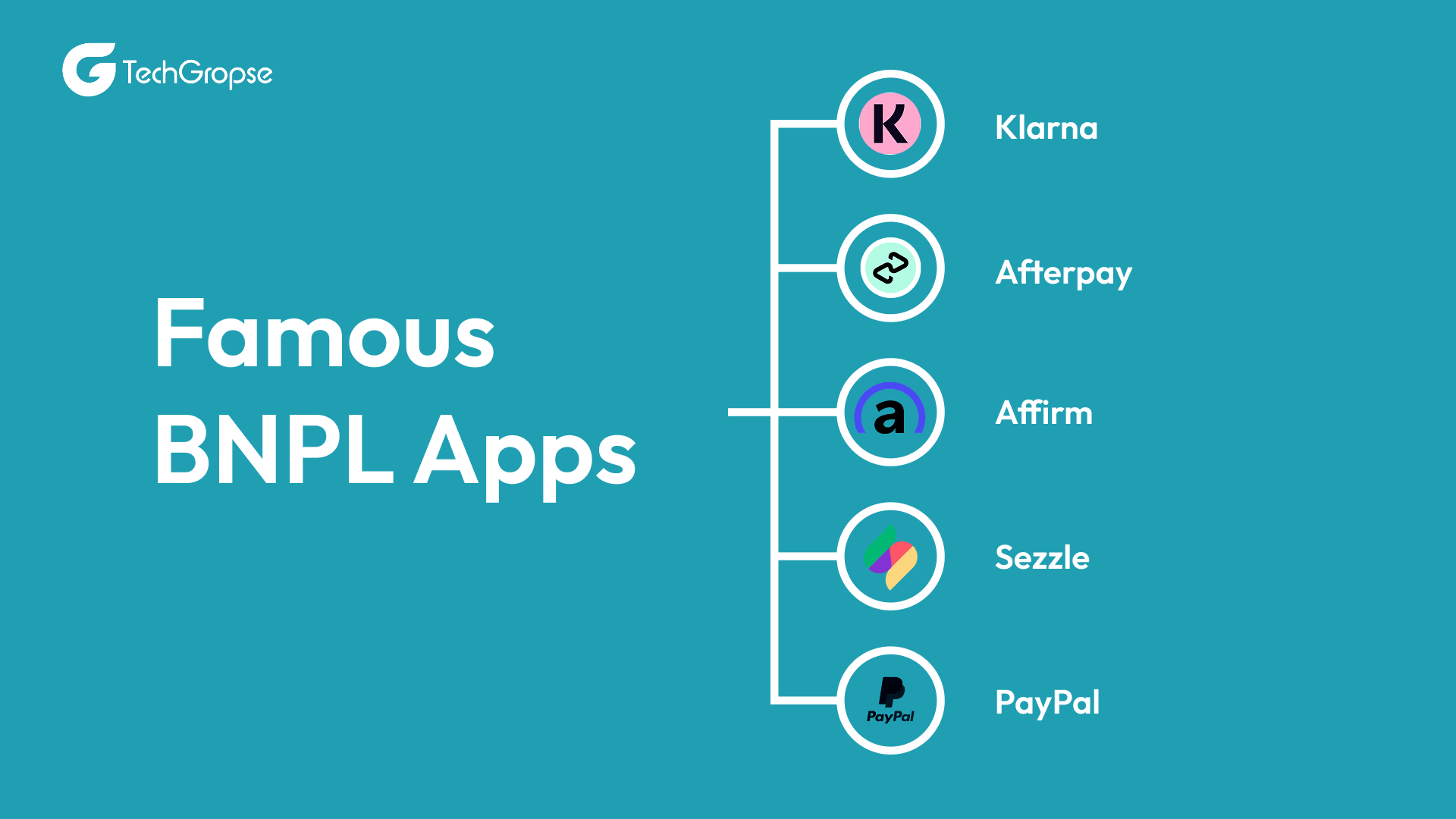

Key Players in BNPL App Development

Before starting the development of a BNPL mobile app, it is imperative to know the major players in it. With this understanding, a business owner or a project manager can assess the scope of it through the major players of BNPL.

-

- Klarna: The Swedish giant that brought BNPL to mainstream consciousness. Klarna offers a wide range of payment options, including “Pay in 4,” pay in 30 days, and longer financing plans. Many businesses want to know the cost to build a BNPL app like Klarna.

- Afterpay: Popular in Australia, the US, and the UK, Afterpay built its dominance on a clean “4 payments, every 2 weeks” model. It targets younger, fashion-forward consumers and has a strong social commerce presence.

- Affirm: More focused on larger, higher-ticket purchases like electronics and travel. Affirm is transparent about interest rates upfront and targets users who want longer repayment terms with clear terms — no hidden fees, no surprises.

- Tabby: Tabby — The Middle East’s leading BNPL platform, Tabby has rapidly become the go-to buy now, pay later solution across Saudi Arabia, the UAE, Kuwait, and Egypt. The FinTech founders can build a BNPL app like Tabby by following a proper procedure.

- Sezzle: A US-based platform that carved out a niche by focusing on underserved credit markets and smaller e-commerce merchants. It also offers a “Sezzle Up” feature that allows users to build their credit score through on-time payments.

What are the Types of Buy Now, Pay Later (BNPL) Apps?

Business founders or key decision makers often confuse the BNPL apps with traditional credit cards or bank loans. However, it is not, and the difference matters a lot for developers.

| Attributes | Credit Card / Loan | BNPL Apps |

|---|---|---|

| Approval Time | Days to Weeks | Matter of Seconds |

| Interest | Zero if Paid On Time | Zero if Paid On Time |

| When Used | General Purpose | At Point of Sale |

| User Experience | Complex | Easy |

| Credit Impact | High Impact | Limited Impact |

What are the Types of BNPL Apps?

According to the budget, a project manager or business owner can choose the kind of BNPL app they want to develop. Only with the correct approach, a business can develop a full-fledged BNPL application.

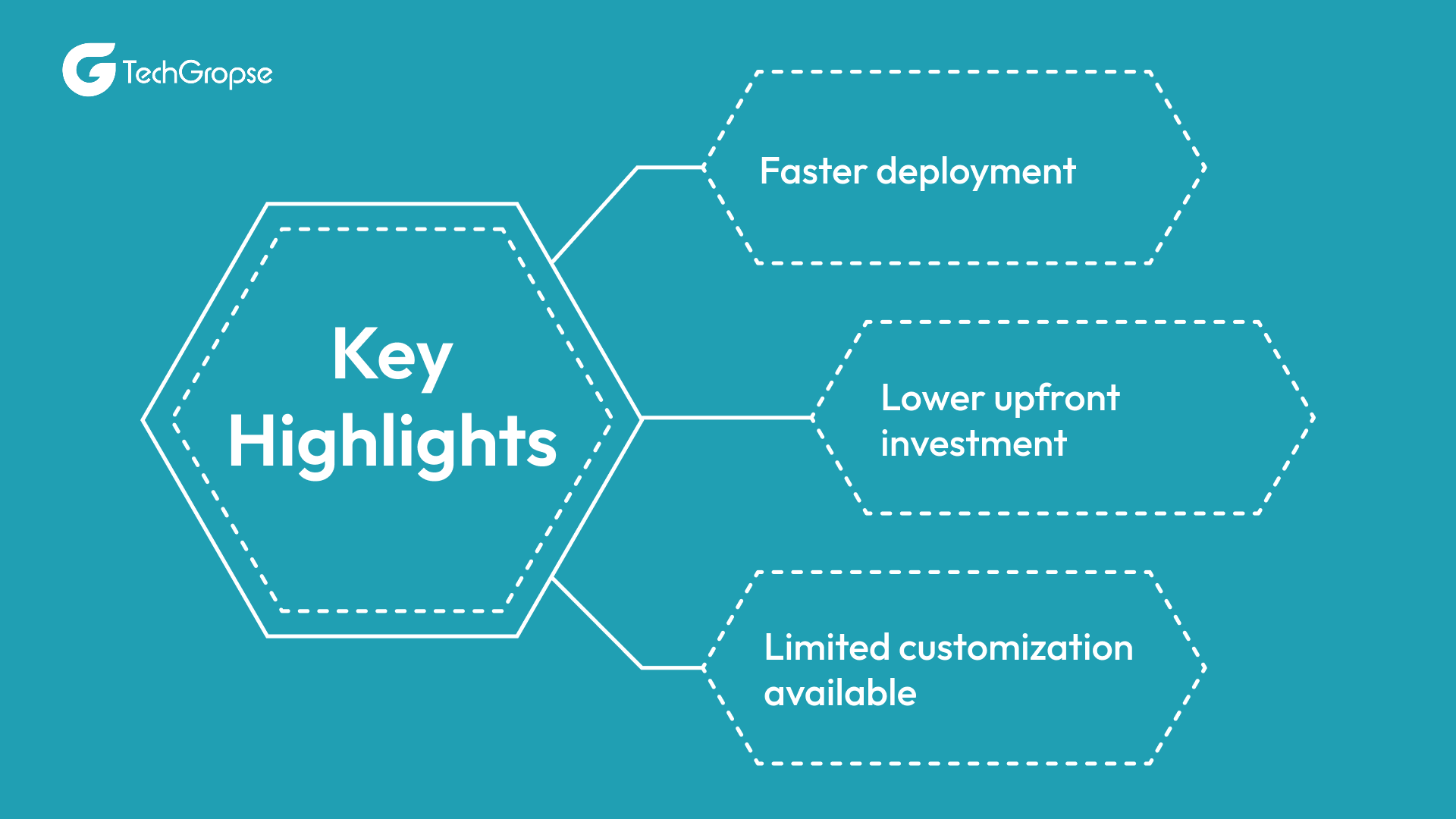

White Label BNPL App Development

A white label BNPL application is a ready-made app developed by a 3rd-party developer or provider. A business can rebrand and use it as its own while the core technology remains the same.

Imagine there’s a fintech startup, and after exploring the BNPL app development cost in India. Instead of building a custom solution, it chose to go with a ready-made app solution.

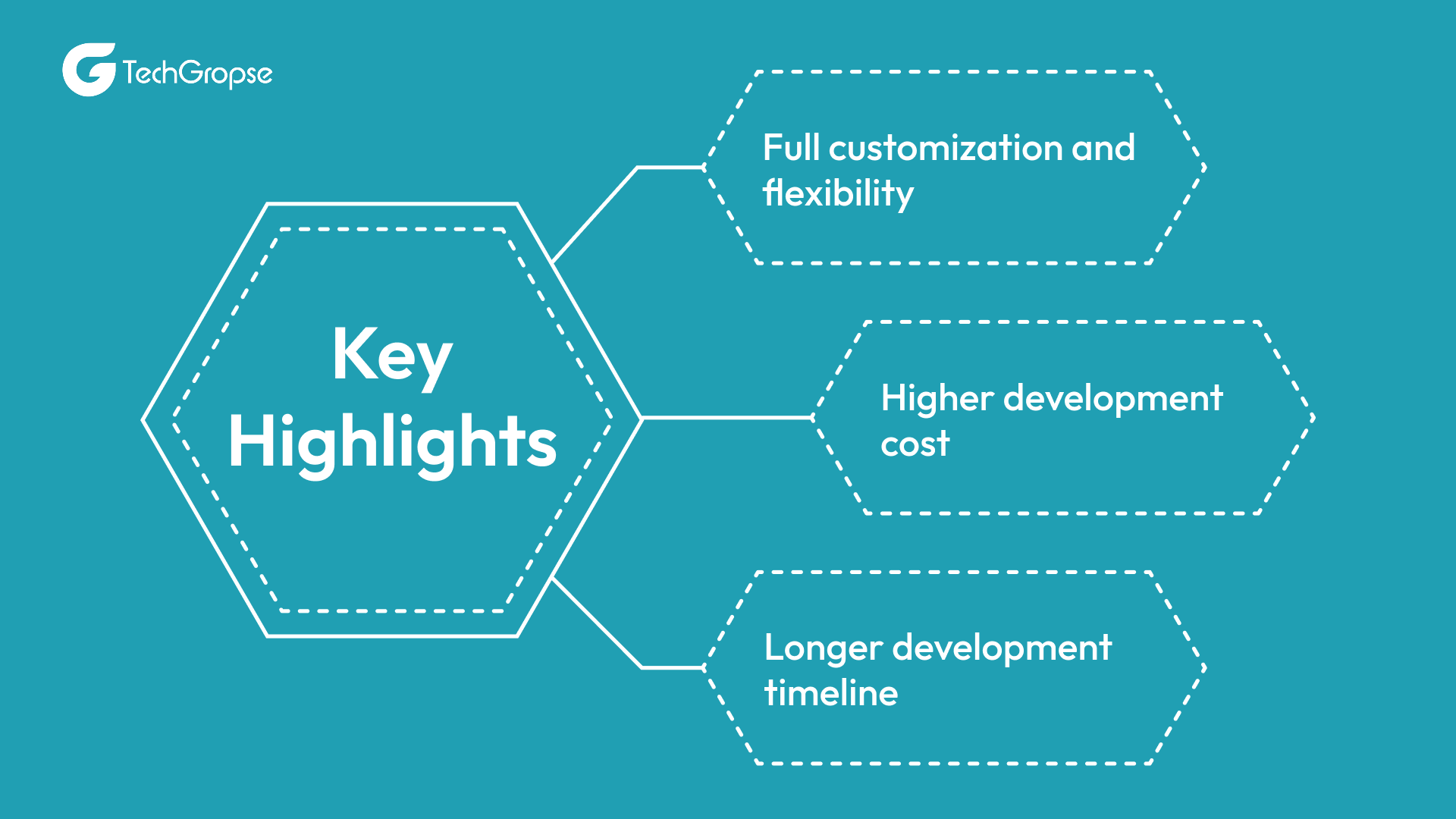

Custom-Built BNPL Platform

A customized Buy Now, Pay Later (BNPL) mobile application is developed according to the specific requirements of a business. Developers building this kind of app have complete control over the features, design, and security architecture.

Again, we will understand it with a simple example of a FinTech startup.

Contrary to the ready-made BNPL app, the startup chose to build an app from scratch with unique functions to serve unique business needs.

Both these BNPL app types come with different cost estimates.

The cost of a white-label BNPL app is lower compared to a customized BNPL mobile app.

In addition, the cost breakdown of a BNPL mobile app is given in the table below:

| App Type | Cost |

|---|---|

| Minimum Viable Product (MVP) | USD 30,000 – USD 60,000 |

| Mid-level BNPL App | USD 60,000 – USD 150,000 |

| Enterprise-grade App | USD 1,50,000 – USD 500,000+ |

What Factors Change the Cost to Build a BNPL App?

The cost of building a BNPL app varies due to operational, technical, and regulatory factors. From app complexity to the developer’s location, many things play a vital role in determining the BNPL app development cost.

App Complexity

The complexity of the mobile app is a crucial factor in deciding the cost of BNPL app development.

A Minimum Viable Product (MVP) only includes essential features of a mobile application. It provides a faster time to market by enabling the startup founder or key decision maker to test the mobile app at a lower upfront investment.

On the other hand, a full-scale BNPL platform includes advanced functionalities like AI-based credit scoring, real-time analytics, fraud detection, multi-merchant support, and financial dashboards. These advanced capabilities increase both development time and cost due to the additional backend infrastructure and security layers required.

Platform Choice (Web, iOS, Android)

The platforms that you decide to deploy your BNPL solution on will affect the cost of development too. When the app is created that will be used in a single platform, i.e., success in Android or iPhone, it will be cheaper.

Nevertheless, in case the businesses need to reach more people, they can create applications on iOS, Android, and web-based platforms at the same time. Multi-platform development needs more facilities, testing & maintenance, and hence it ends up consuming more funds in the development budget.

Tech Stack Decisions

The development cost also depends greatly on the technology stack to be employed in the frontend, the backend, and the database. The decisions to utilize new technologies like cloud architecture, scalable database, and secure frameworks on the back-end might involve hiring skilled programmers and expert skills.

Besides, the choice of tools used in data processing, security policies, and the payment processing system can also influence the overall cost of development. A strong tech stack is going to be scalable and secure, and can cost more to develop in the beginning.

In-House Team vs. Outsourcing vs. Hybrid model.

The cost determination is also influenced by the approach applied in development. When companies develop an in-house development team, it requires them to invest in the hiring of competent developers, designers, testers, and project managers, whichh add to their operational costs.

Alternatively, the project can be outsourced to an application developer company that will save the infrastructure and staffing expenses and provide a pool of professionals. Certain companies implement a hybrid approach, in which development of core business processes is in-house, but other specialized work is outsourced.

Geography of Your Development Team

The placement of the development team is a major determinant of the hourly rate of development. As an illustration, a developer in North America and Western Europe would normally demand a higher price than a development team at a certain region like Asia or Eastern Europe.

A lot of companies turn to outsourcing the development of BNPL to a country that has good technological skills and offers favourable prices that do not affect quality.

Third-Party Integrations

BNPL applications are highly dependent on the external services to be effective. Such integrations can be payment gateways, credit bureaus, identity verification systems, or KYC, fraud detection tools, and analytics tools.

All the third-party services have to be integrated by API, tested, and maintained. There are also some services that have a transaction fee or subscription, which adds up to the overall development and operation cost.

Regulatory Requirements and Compliance Requirements

The BNPL apps are located within the financial technologies (fintech) market and, therefore, should be subject to strong regulations. The compliance steps that businesses have to take include data protection protocols, financial reporting procedures, anti-money laundering (AML), and KYC authentication systems.

These regulatory requirements can include new security infrastructure, legal advice, and compliance tests, which can add to the cost of development but are required to ensure trust and prevent legal liability.

Moreover, a startup can hire BNPL app developer, and its location & experience matter a lot. These influence the cost of BNPL app development in the year 2026.

How to Reduce BNPL App Development Costs Without Cutting Corners?

Developing a Buy Now, Pay Later (BNPL) application may be a costly undertaking, particularly because of security, compliance, and financial integrations. Nevertheless, the cost of development can be reduced in a strategic manner by a business without reducing quality and functionality.

Using the proper development strategy and technology selection, organizations will have the opportunity of optimizing their finances and continue to create a scalable BNPL system.

The following can be considered as some of the useful methods of minimizing the cost to build a BNPL app without compromising performance or reliability.

Start with an MVP

A Minimum Viable Product (MVP) is one of the best methods of managing development costs. Rather than designing a complete platform at the beginning, an MVP is based on the main features that the functioning of the app needs.

As an illustration, BNPL originally could comprise user registration, payment schedule, monitoring of transactions, and simple integration with merchants. When the product starts gaining traction and user feedback is received, they can also add new functionality such as advanced analytics, AI-based credit scoring, and loyalty programs, afterward, in updates.

Releasing MVP enables businesses to test their model and ensure reduced cost to build a BNPL app, as well as boost time-to-market.

White-Label Solutions for the beginning stages

By leveraging white-label BNPL solutions, early-stage startups can save a substantial amount of time and money in development and get to the point of development much sooner. They are ready-made platforms that have been created and offered by third parties and can be tailored by the businesses to fit their branding and interface.

Companies can develop their BNPL app in no time using a ready-made framework instead of developing a complete system. The solution is one that reduces the intensity of resources required in its development, but allows businesses to provide flexibility in payment services to their clients.

A white-label solution can be effective to assess market demand and invest in a fully-customised BNPL platform.

Take Advantage of Open-Source Components

Open-source technologies and frameworks may enable the reduction of licensing fees and cost to build a BNPL app. Numerous open-source software have been popular in fintech applications and offer credible performance, scalability, and community value.

As an example, the frameworks that may be developed using open-source can be an example of backend development, data management, and API integrations. This enables the developers to develop strong applications without necessarily having to use costly proprietary software.

It should, however, be noted that the open-source pieces have to be secured, updated on a regular basis, and in adherence to financial industry standards.

Hire Seasoned Fintech Developers

Another way of optimizing the cost to build a BNPL app is by collaborating with more experienced Fintech developers or special development firms. Competent teams already know the ins-and-outs of financial applications, such as processing payments, fraud detection, regulatory compliance, and data protection.

Their expertise reduces the risk of costly errors, delays, and security vulnerabilities during development. Experienced developers can also recommend the most efficient technology stack and architecture, helping businesses avoid unnecessary expenses.

As a result, working with the right development team often leads to faster development cycles and better long-term scalability.

You May Also Like: AI App Development Cost

How TechGropse Can Help Build A Buy Now, Pay Later (BNPL) App?

TechGropse is a trusted BNPL mobile app development company with experience in creating custom mobile apps. These apps follow compliance rules and are feature-rich.

Our developers are skilled and have multiple years of experience in building robust mobile apps. Our developers are skilled and can build mobile apps with multiple years of experience. The following points showcase the importance of TechGropse for development and the reduction of cost to build a BNPL app:

- Build apps with dedicated resources by creating a wireframe to build BNPL mobile apps.

- Deliver BNPL like apps before the deadline to facilitate easy testing of mobile apps.

- The solutions we build come with mandatory after-sales support with a ticket management system.

- Apps are developed mostly within a pre-decided budget and time using the new-age technologies.

Conclusion

The market of Buy Now, Pay Later (BNPL) is growing at a quick pace due to the evolving tastes of consumers and the popularity of Millennials and Gen Z, who are more conscious about flexible and convenient payments.

For businesses and fintech startups, creating a BNPL app is no longer a choice, but a business necessity to seize a growing market and engage customers. But the decision-makers are indecisive due to their inability to assess the exact cost to build a BNPL app.

Although the price at which development is done depends on several factors, such as the complexity of the apps, platform used, technology stack, integrations, and compliance requirements, the businesses can still work out the costs in a strategic way without hampering quality.

A white-label solution, an MVP, and open-source technologies, alongside collaborating with established fintech developers, are effective strategies to reduce costs for building a BNPL app.

For more information about the cost to build a BNPL app, contact TechGropse. You can contact TechGropse by sending an email to info@techgropse.com.

Frequently Asked Question (FAQs)

A BNPL (Buy Now, Pay Later) app allows users to purchase products or services immediately and pay for them in installments, often with zero interest if payments are made on time. It provides a flexible alternative to traditional credit cards or loans.

- White-label BNPL apps – ready-made apps that can be rebranded.

- Custom-built BNPL platforms – developed from scratch for unique business needs.

- BNPL as a feature – integrated into an existing fintech or eCommerce app.

Cost-saving strategies include:

- Starting with an MVP to test the market

- Using white-label solutions for early-stage deployment

- Leveraging open-source components

- Working with experienced fintech developers to avoid costly mistakes

Yes. BNPL apps fall under the fintech and digital payments sector, so they must adhere to regulations like KYC (Know Your Customer), AML (Anti-Money Laundering), data protection, and financial reporting standards. Compliance ensures security and builds user trust.

Absolutely. BNPL apps can:

- Increase conversion rates and average order values

- Improve customer loyalty and retention

- Open new revenue streams through merchant fees, interest, or subscription models

Development timelines vary:

- MVP: 3–4 months

- Mid-level BNPL app: 5–8 months

- Enterprise-grade solution: 8–12+ months

Timelines depend on features, platform selection, integrations, and regulatory compliance requirements.

Hello All, Aman Mishra has years of experience in the IT industry. His passion for helping people in all aspects of mobile app development. Therefore, He write several blogs that help the readers to get the appropriate information about mobile app development trends, technology, and many other aspects.In addition to providing mobile app development services in USA, he also provides maintenance & support services for businesses of all sizes. He tried to solve all their readers' queries and ensure that the given information would be helpful for them.