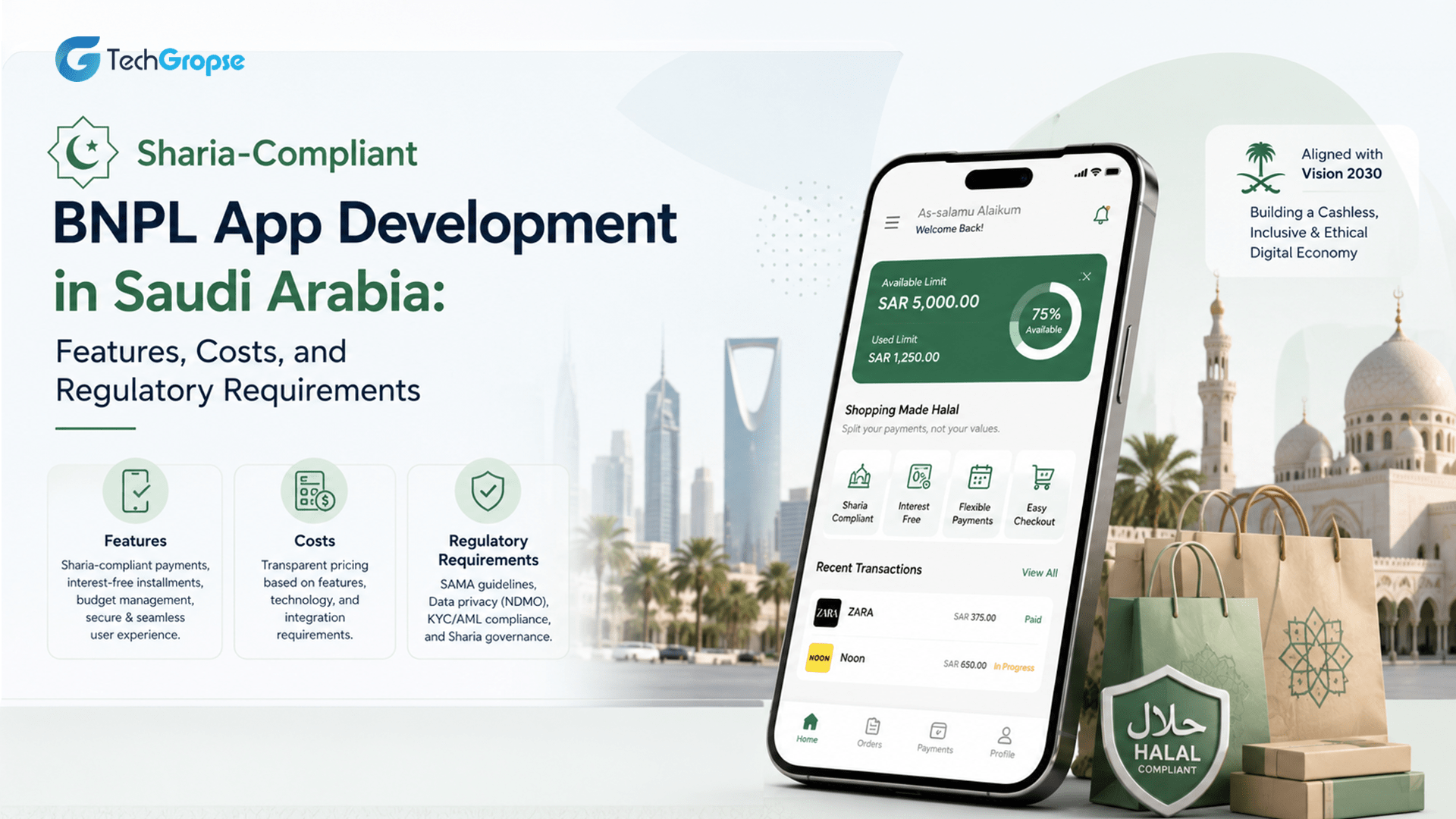

The Buy Now Pay Later (BNPL) application industry has revolutionized digital payments globally. However, in Saudi Arabia, the concept of BNPL has taken a different approach by developing Sharia-compliant systems in accordance with Islamic laws. Due to increasing consumer awareness about ethical practices, companies are now spending substantial time on Sharia-compliant BNPL App Development to cater to customers’ demands.

Due to the presence of a flourishing ecosystem of fintech firms, initiatives by the government, and the high rate of smartphone usage in Saudi Arabia, there exists an excellent opportunity for BNPL app development that satisfies all requirements of Islamic finance.

In this blog, we will discuss the market opportunity, features, development process, compliance considerations, and costs involved in developing Sharia-compliant BNPL app development in Saudi Arabia.

Key Takeaways:

- What is Sharia-Compliant BNPL App Development?

- Market Scope of Sharia-Compliant BNPL App Development

- Why Sharia-Compliant BNPL App Development is Growing in Saudi Arabia?

- Islamic Principles Behind Sharia-Compliant BNPL App Development

- Essential Features of a Sharia-Compliant BNPL App Development Project

- Step-by-Step Process of Sharia-Compliant BNPL App Development

- Cost of Sharia-Compliant BNPL App Development in Saudi Arabia

- Conclusion

- FAQs (Frequently Asked Questions)

What is Sharia-Compliant BNPL App Development?

The concept of Sharia-Compliant BNPL App Development relates to the development of BNPL platforms following the rules of Islamic financing. Conventional BNPL apps may be associated with interest rates and penalties for delayed payment, whereas Islamic financing BNPL platforms follow the permitted modes of financing, including Murabaha.

In the Murabaha arrangement, the fintech company buys the asset and sells it to the consumer at a disclosed markup. In return, the consumer makes payments through installments with no interest involved.

Thus, the Sharia-compliance rule is followed while offering flexible payment plans to consumers. Therefore, Sharia-compliant Fintech App Development is gaining significance in Saudi Arabia.

Market Scope of Sharia-Compliant BNPL App Development

According to Statista, Saudi Arabia’s BNPL transaction value is expected to continue growing through 2031, supported by a projected CAGR of 20.8% between 2026 and 2031.

Data from Grand View Research says that the global BNPL market is expected to grow from USD 11.87 billion in 2025 to USD 80.15 billion by 2033, creating strong momentum for regional BNPL platforms.

Another research by Statista says that the Saudi BNPL market recorded a 28% CAGR between 2022 and 2025, highlighting rapid consumer adoption of installment-based payments.

Why Sharia-Compliant BNPL App Development is Growing in Saudi Arabia?

Sharia-Compliant BNPL Application Development has started picking up pace in Saudi Arabia owing to the swift rise in digital payment trends, an increase in the usage of e-commerce platforms, and a growing need for Islamic financing products. The requirement for flexible payment methods with no interest-based transactions, along with government-backed fintech innovations, has fueled its growth.

Rise of Digital Ecosystem

The growth of the digital landscape, the increasing number of smartphones, and the rising popularity of e-commerce in Saudi Arabia have made it essential to adopt more flexible payment options. The growing trend of using applications for online purchases and other monetary transactions has motivated companies to invest in Buy Now Pay Later App Development in Saudi Arabia.

Sharia-Compliant Payment Solutions

Many people in Saudi Arabia tend to have a preference for financial products that conform to Islam’s guidelines. Sharia Compliant Payment Solutions offer financing without interest charges within an ethical framework that is transparent.

Government Support for Fintech App

The Saudi government has been playing an active role in promoting fintech innovations through initiatives like those of Vision 2030. The conducive environment created by these developments has helped the growth of Saudi Fintech App Development and made firms develop compliant digital financial services.

Buy Now Pay Later App Development

The increasing need for flexible payment options in areas like retail, healthcare, education, and travel is promoting the uptake of BNPL services. The use of BNPL platforms through Islamic financing models has been found to attract more customers and present new business prospects within Saudi Arabia.

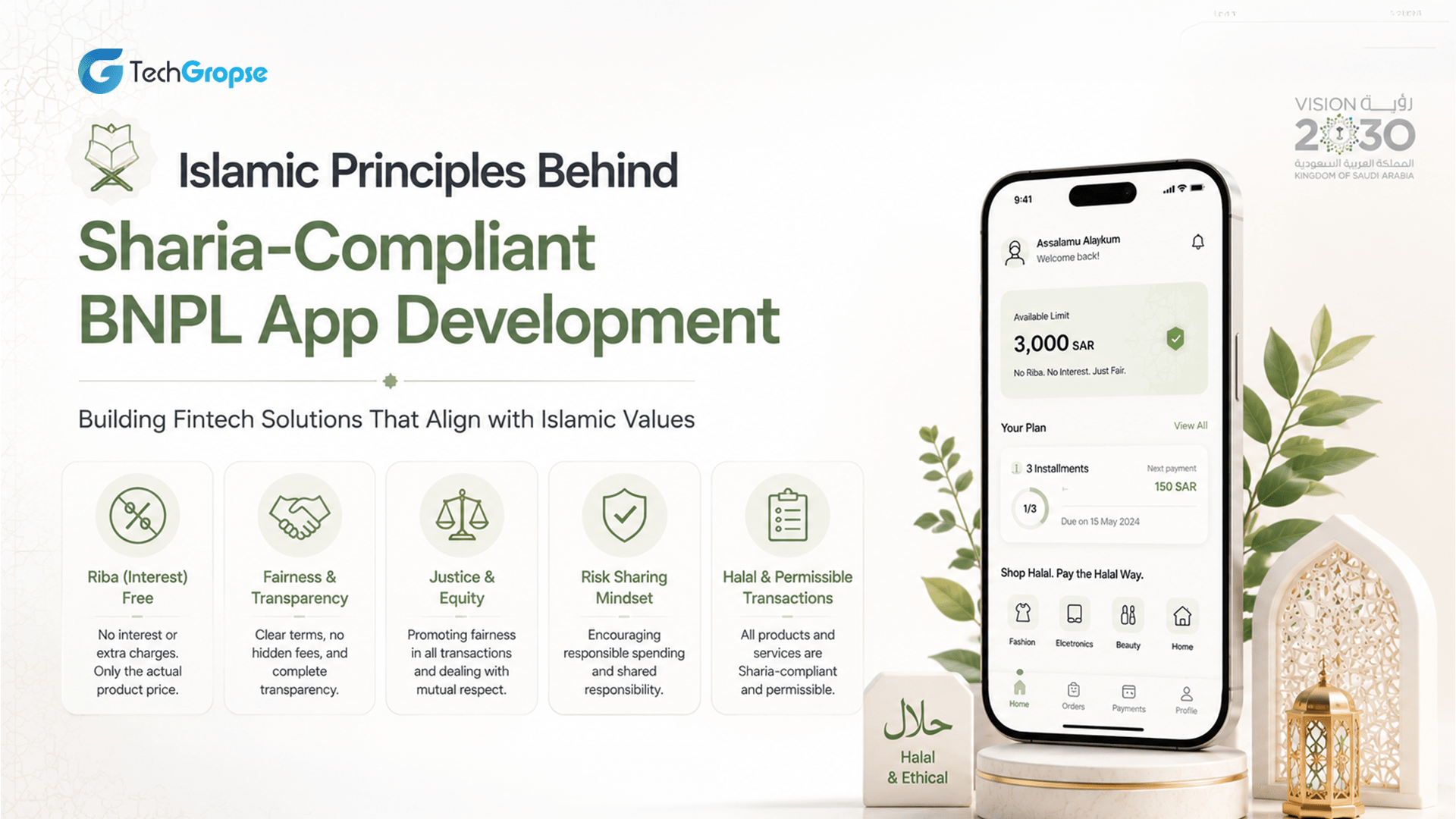

Islamic Principles Behind Sharia-Compliant BNPL App Development

Development of Sharia-Compliant BNPL Apps entails creating applications based on Islamic finance laws, which ensure that all monetary dealings are ethical, transparent, and devoid of any form of interest. Such an application enables people to make payments through the best available means of financing without breaching any of the provisions in the Sharia law. The incorporation of accepted methods of Islamic financing, for instance, the Murabaha financing model, enables the service provider to create a convenient method of payment for consumers.

Prohibition of Riba (Interest)

One of the main principles of Islamic finance is that there should be no Riba, which implies the act of paying or taking interest in any type of financial dealings. As interest-based lending is against Sharia, BNPL companies based on Sharia principles cannot charge their customers any form of interest or penalty in case of delayed payments. They earn money through the use of Islamic modes of financing such as Murabaha.

Asset-Backed Financing

Islamic finance mandates that all transactions in financial terms must necessarily have a link to some asset, product, or service. This means that the financing processes are grounded in reality rather than being speculative or uncertain. In the case of BNPL finance under the Islamic system, it usually starts with the purchase of the product by the service provider for the customer. It is subsequently sold by the service provider at a profit.

Transparency and Fair Contracts

Transparency is an essential element in the Islamic financial system. Each financing contract needs to make known to the clients some key elements such as the cost of the commodity, the rate of profit, the payment method, the time of payment, and the amount of commission. The clients need to know their obligations before making the decision to agree to a particular transaction.

Risk Sharing and Ethical Financing

The Islamic banking system upholds the notion of fair trade and ethics in trade by promoting the distribution of risks among both the provider and the customer. The distribution ensures that all parties have equal risks, instead of putting all the financial burden to one of the trading parties, thus preventing any form of exploitation.

Murabaha-Based BNPL Solutions

Murabaha-Based BNPL Solutions are one of the most widely adopted forms of finance for Islamic BNPL platforms. In this form of finance, the service provider buys the required goods first and later sells it to the consumer at a profit that is predetermined and made fully known to the consumer before any sales. The consumer pays back the entire amount through installment payments over a predetermined period of time. Since the profit is predetermined and there are no interests involved, this type of financing is completely Sharia-compliant.

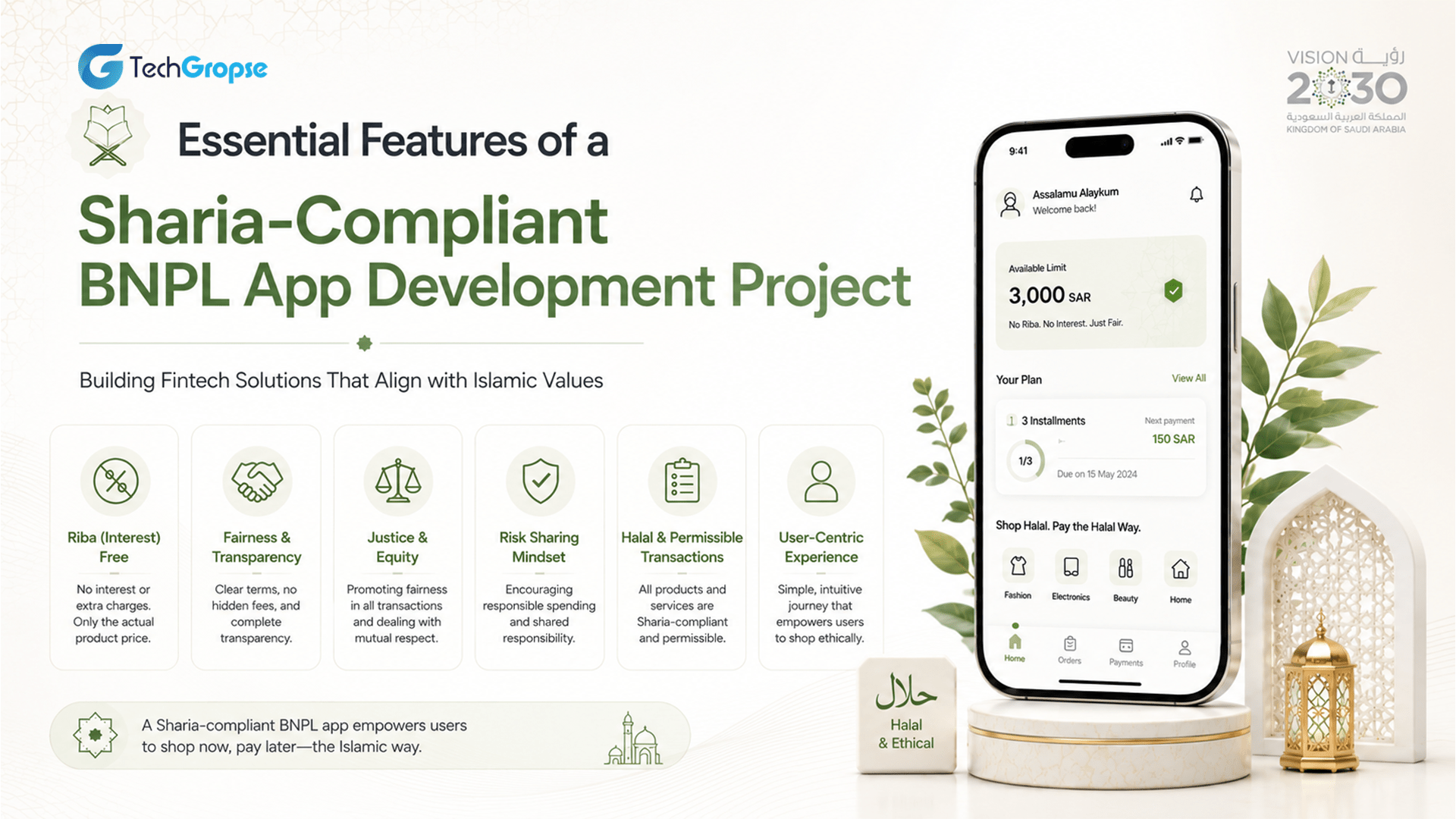

Essential Features of a Sharia-Compliant BNPL App Development Project

For an effective BNPL app that is Sharia-compliant, the following three aspects should come together: state-of-the-art fintech solutions, highly secure payment systems, and Sharia-compliance mechanisms. In such a way, users will be provided with a seamless experience, and the system will remain transparent, secure, and effective. With the help of these elements, companies will be able to create BNPL solutions.

User Registration and Digital Onboarding

There is a need for a user-friendly sign-up process which would make account creation easier and faster for the users. The use of features like mobile verification, biometrics, and uploading documents could aid in making the account creation process more convenient and secure.

Secure KYC and Identity Verification

Effective KYC procedures will assist with verifying the client’s identity, preventing any fraud, and ensuring compliance with local legislation. Modern techniques such as OCR-driven document scans, biometric authentication tools, and live identity checks can enhance protection and ensure adherence to the local financial regulations.

Merchant Management Portal

The merchants need a dedicated portal that will assist them in managing products, tracking transactions, recording settlements, and accessing customer information. The portal will also offer the merchant analysis regarding sales, finance, and transaction history to assist them in optimizing business processes.

Murabaha-Based Financing Engine

This is the key feature of Islamic BNPL App Development. Financing Engine automates purchases of assets, markup determination, repayments, and documentation. This makes sure that all transactions adhere to the accepted rules of Islamic financing. At the same time, transparency is assured for merchants and their clients.

Flexible Installment Management

It will be necessary for customers to check their payment plans, the payment deadlines, their balance, and transactions on a unified dashboard. Flexibility in the installments helps increase customer satisfaction, since it gives customers more freedom and flexibility while making payments.

AI-Powered Credit Assessment

By analyzing customer spending patterns and transactional behaviors, artificial intelligence can be used to determine customer suitability. This leads to prudent lending practices, reduces the risk of default, and makes the entire procedure more efficient without compromising the customer experience.

Sharia Compliance Monitoring Dashboard

Through a separate dashboard, compliance officers and Sharia consultants are able to track transactions to ensure their alignment with the principles of Islam. This dashboard can also be used to produce audit reports and trace financing operations in real time.

Payment Gateway Integration

In order to make the process of making payments possible, a reliable payment gateway system must be implemented by the system. It should be capable of accepting different modes of payment such as debit cards, bank transfers, and online wallets.

Customer Notifications and Reminders

Automated notifications help the user keep track of the payment schedule, approval process, transaction updates, and upcoming installments. Notifications are important to enhance customer interaction and avoid missed payments.

Analytics and Reporting Tools

The benefits of advanced analytics include understanding customer actions, repayment behaviors, merchant activities, and how to generate revenues. Such tools help organizations make informed decisions in the areas of financing, growth, and improving platform performance.

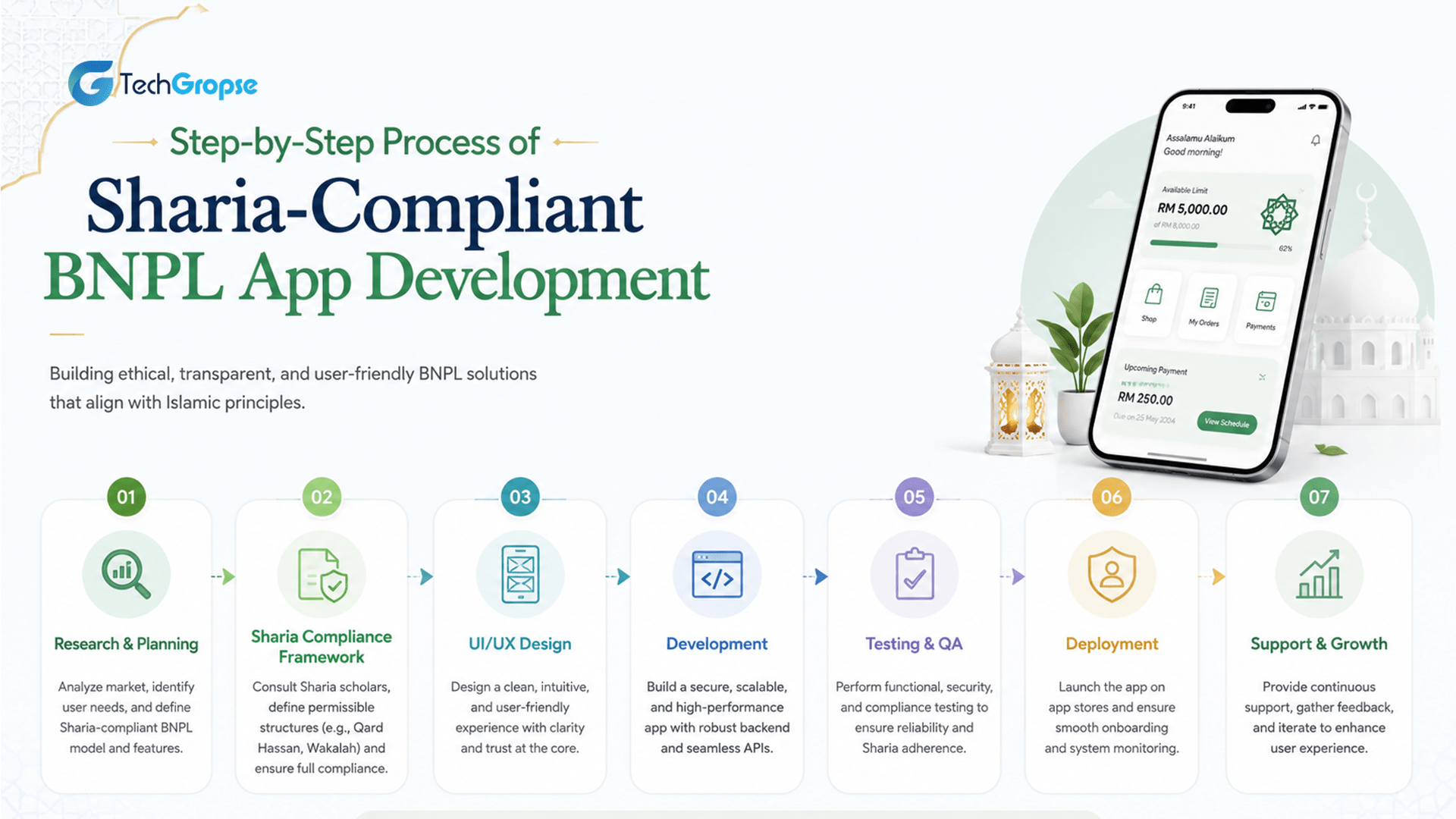

Step-by-Step Process of Sharia-Compliant BNPL App Development

For the development of a Sharia-compatible BNPL solution, there is a need to consider certain steps for the development to be successful. The process involves several stages, including research, assessing regulations, development, testing, and deployment, among others, which are all important for ensuring that the system is secured and scalable. It should also be developed in line with the Sharia guidelines. The importance of following this stepwise approach cannot be understated.

Market Research

The development process starts with an extensive market study that will help the business in comprehending the customer expectations, competitors’ strategies, the gap in the market, and upcoming trends in fintech in Saudi Arabia. Such information will enable the company to come up with a BNPL system in line with customer preferences and needs.

Regulatory Assessment

Before the commencement of development, the business must perform a complete regulatory assessment. This includes assessing license-related conditions, data protection, consumer protection, anti-money laundering, and SAMA BNPL Regulations. Compliance will minimize risks and ease the process of gaining approvals.

UI/UX Design

A good user interface design is crucial to the success of any BNPL service. The process of developing UI/UX is about designing the interface to be clear and attractive in making users register accounts, finance requests, payment tracking, and installments management.

Core Development

Core development encompasses creating basic functionality for the platform, such as functions for managing users, onboarding merchants, financing, payments, compliance monitoring, and reports. The core phase serves as the bedrock for the BNPL application, providing smooth running of the entire application.

Payment Gateway

Secure payment gateway integration is important because it facilitates easy transactions. Integrating a reliable payment gateway and APIs from banks helps in handling installment payments, settlement of merchants, and multiple payment options.

Security Testing

The main reason for security testing is to look for any possible weaknesses so that the sensitive information can be safeguarded. Penetration testing, testing the security of encrypted data, assessing fraudulent transactions, and compliance testing are some of the types of security tests conducted on the platform.

Approval Process

Following the development and tests for the platform, the application has to receive the relevant approvals from the authorities concerned with both regulation and Shariah. Approvals in this respect will ensure that the application abides by all financial regulations and rules of Islamic finance before going public.

Deployment & Maintenance

The platform is released into production after getting necessary approvals and becomes accessible to the users. Some of the key areas covered by the maintenance team include performance, security updates, new feature development, compliance and management, and technical support for maintaining security and efficiency in scaling the operations.

Cost of Sharia-Compliant BNPL App Development in Saudi Arabia

BNPL Application Development Cost for Sharia-Compliant Services in Saudi Arabia depends on various elements, including the degree of complexity of the app, features required, integration with other applications, security standards, Sharia-compliance implementation, and other customizations needed. Further expenses might include obtaining regulatory approvals, Sharia-compliant audit fees, cloud hosting services, and maintenance charges.

Simple

A typical Sharia-based BNPL system development price ranges from SAR 93,750 – SAR 187,500. Such software normally consists of fundamental modules including user registration, initial KYC checks, merchants onboarding, payments monitoring, and integration with regular payment systems. The system suits startups that are at the stage of developing a business case and want to test market demand without spending too much.

Advanced

A sophisticated BNPL system will cost between SAR 187,500 – SAR 450,000 . Apart from the basic features, it has AI-driven credit scoring, analysis tools, merchant integration, secure payment processing, compliance dashboard, among other features. Such systems are meant for startups and fintech companies looking to scale up their operations, reduce risks and improve their customer experience.

Complex

Enterprise-ready solutions with full customization will cost from SAR 450,000 – SAR 1,125,000+ based on the complexity of the project and the technology used. They will be built with an engine that enables Murabaha financing, real-time integration with the bank’s system, enterprise-level security, multilingual capabilities, robust reporting, and automated compliance management systems. Such a system is ideal for banks, financial institutions, and large fintech companies wishing to offer highly secure, scalable, and Sharia-compliant financing options.

| Development Level | Estimated Cost (USD) | Estimated Cost (SAR) | Timeline | Ideal For | Key Features |

|---|---|---|---|---|---|

| Simple BNPL App | $25,000 – $50,000 | SAR 93,750 – SAR 187,500 | 3–5 Months | Startups & SMEs | User Registration, KYC, Basic Installment Plans, Payment Gateway Integration, Merchant Dashboard |

| Advanced BNPL App | $50,000 – $120,000 | SAR 187,500 – SAR 450,000 | 5–8 Months | Growing Fintech Businesses | All Simple Features + AI Credit Scoring, Merchant Management, Analytics, Multi-Language Support, Enhanced Security |

| Complex Enterprise BNPL App | $120,000 – $300,000+ | SAR 450,000 – SAR 1,125,000+ | 8–14+ Months | Banks, Fintech Enterprises & Large Retailers | All Advanced Features + Murabaha-Based Financing Engine, Open Banking Integration, Advanced Risk Management, Fraud Detection, SAMA Compliance Framework, Scalable Cloud Infrastructure |

Conclusion

Sharia-Compliant BNPL App Development can turn out to be a promising area of development for entrepreneurs due to the rise of fintech innovations in Saudi Arabia. Consumers’ need for more ethical, trustworthy, and interest-free loan products can bring many benefits for your business when creating an innovative solution.

Utilizing such concepts as Murabaha-Based BNPL Solutions and complying with SAMA regulations will help businesses establish an effective platform capable of fulfilling all users’ needs and expectations.

No matter whether you are a startup, a fintech provider or a financial institution, it would be a good decision to consider the implementation of an Islamic BNPL App Development in Saudi Arabia, where it will contribute to further development of the sector.

Are you considering BNPL App development to attract customers with your Sharia-compliant product? Get in touch with our experienced fintech software developers to create a reliable platform from scratch.

FAQs (Frequently Asked Questions)

Creating a Sharia-compliant BNPL product involves creating an app which will enable customers to make their payments using installment loans without having to pay interest (Riba). Sharia-compliant BNPL products use Sharia-compliant financial instruments, such as Murabaha.

The difference between Sharia-compliant and non-Sharia BNPL apps is that while a Sharia-compliant BNPL app makes use of Sharia-compliant payment procedures, a non-Sharia BNPL app might have interest among others.

Some features to expect from Sharia-Compliant BNPL platforms would be: online onboarding, KYC check, financing through Murabaha, installment management, payments gateway, compliance management and analytics dashboard.

BNPL providers need to ensure compliance with SAMA regulations regarding licensing, consumer protection, AML policy, data security measures, disclosure of financing and many other important aspects.

Murabaha-based BNPL solutions ensure compliance with Sharia by purchasing an asset on behalf of the borrower and selling it to him/her at a clearly defined profit margin.

The expenses required to develop a BNPL platform depend on its complexity and begin from SAR 93,750 for a basic application up to SAR 1,125,000 and above for a complicated one.

Depending on complexity, basic platforms will be developed during 3-4 months, while complicated solutions may take 6-12 months, and sometimes even more.

Some key aspects to pay attention to include: data encryption, security authentication, AML requirements, KYC validation, anti-fraud tools and other cybersecurity rules of the country of operation.

The main issues that must be considered include compliance, Sharia-compliance, anti-fraud measures, customer risk analysis, and payment system integration.

There are several reasons why Saudi Arabia is becoming the most promising destination for fintech app development including its strong digital ecosystem.

Hello All, Aman Mishra has years of experience in the IT industry. His passion for helping people in all aspects of mobile app development. Therefore, He write several blogs that help the readers to get the appropriate information about mobile app development trends, technology, and many other aspects.In addition to providing mobile app development services in USA, he also provides maintenance & support services for businesses of all sizes. He tried to solve all their readers' queries and ensure that the given information would be helpful for them.