In 2025, the Global Islamic Fintech Market was valued at AED 818.30 billion. However, the majority of the currently existing fintech infrastructure was developed on the principles of traditional banking, interest-based transactions, speculation, and the design of debt-based products. The space is challenging for developers and companies that are entering the field, yet it is an opportunity at the same time.

This article explains the architecture, feature requirements, integration patterns, cost considerations, and how to scale across multiple markets from a technical and structural point of view for Shariah-Compliant Platform Development.

What Is Shariah-Compliant Platform Development?

According to a study by Grand View Research, the global Islamic fintech market was valued at USD 222.97 billion in 2025 and is projected to reach USD 619.20 billion by 2033, growing at a 13.8% CAGR. The report highlights increasing demand for Shariah-compliant digital banking, halal investment platforms, Islamic BNPL solutions, and cloud-native fintech infrastructure across the Middle East and Asia-Pacific.

A report published by Allied Market Research states that the global Islamic finance market is expected to grow from USD 2.5 trillion in 2023 to USD 7.7 trillion by 2033, at a 12% CAGR. The study identifies rising consumer preference for ethical and interest-free financial systems as a major driver behind the demand for Shariah-compliant digital platforms and fintech ecosystems.

A 2025 academic study titled “The Evolution of Global Islamic FinTech: Market Dynamics, Concentration and Consolidation of the Product Structure” published on ResearchGate explains how Islamic fintech has evolved into a distinct global financial ecosystem. The research emphasizes that future growth opportunities lie in scalable Shariah governance, regulatory technology, AI-powered Islamic banking, and digital investment platforms tailored for underserved Muslim populations worldwide.

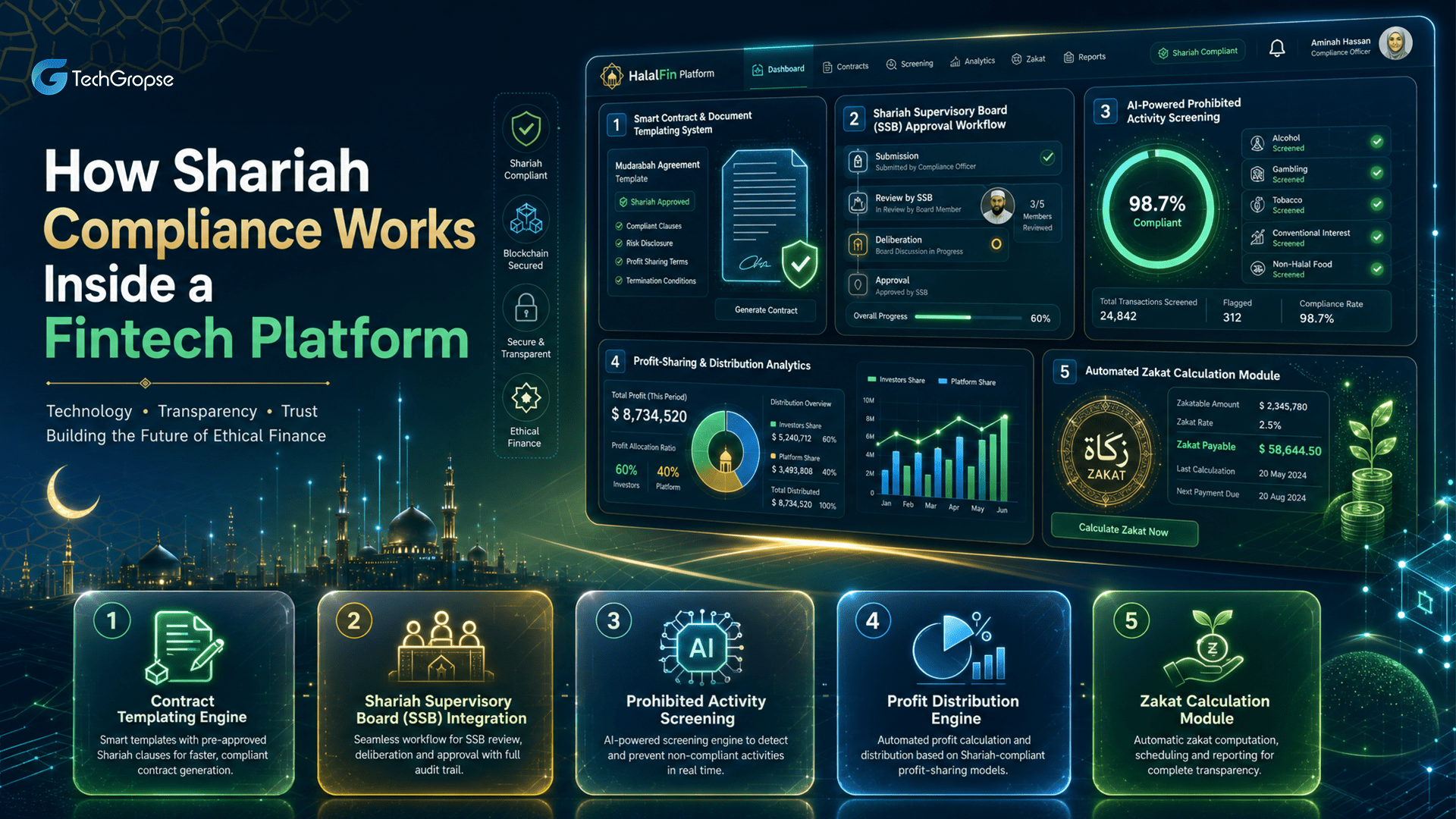

How Shariah Compliance Works Inside a Fintech Platform

It is important to grasp the notion of Shariah compliance as a technical requirement and not merely a legal requirement, as this will differentiate platforms that are actually serving Islamic finance and those that are only rebranding conventional products. This section discusses how compliance principles apply to engineering decisions within the platform.

The most mainstream fintech platforms are designed on a ledger that has debits and credits and an interest computation motor. In the Islamic platform, this structure is replaced by or wrapped in contract-based logic.

Let’s see what compliance is translated to the platform:

Contract Templating Engine: All financial products, finance, savings, investments, insurance etc. are mapped to a named format of Islamic contract (Murabaha, Musharakah, Wakalah, Takaful, etc.). These are held on the platform as “parameterized” contract templates, which have a set of pre-established approval sequences.

Shariah Supervisory Board (SSB) Integration: Platforms that are most serious provide an SSB review layer in their approval processes: New products, contract changes and edge-case transactions go into a review queue which can be accessed by the SSB. The audit trail is saved on a per-contract basis, not per transaction.

Prohibited Activity Screening: Investment and Financing products – the platform performs sector screening on the company databases. Some of the typical exclusions are alcohol, tobacco, conventional financial services, adult entertainment, and products containing pork. Screens are generally rule-based, but are also being increasingly classified using NLP.

Profit Distribution Engine: The platform works on a profit distribution engine rather than interest accrual, and calculates and distributes profit according to the agreed ratio and the actual performance of the fund. This necessitates a more complex accounting system than the fixed-rate accrual, especially in Musharakah and Mudarabah.

Zakat Calculation Module: There are several Islamic fintech platforms that have an integrated zakat calculation module. This isn’t a little extra. Zakat is calculated on the assets that are above a certain threshold (nisab) for a specific period of one lunar year, with different rates for different types of assets. A suitably designed Zakat Platform Development module facilitates multiple asset portfolios, adjusts for lunar calendar-based dates, and enables the person to specify the beneficiaries of the Zakat.

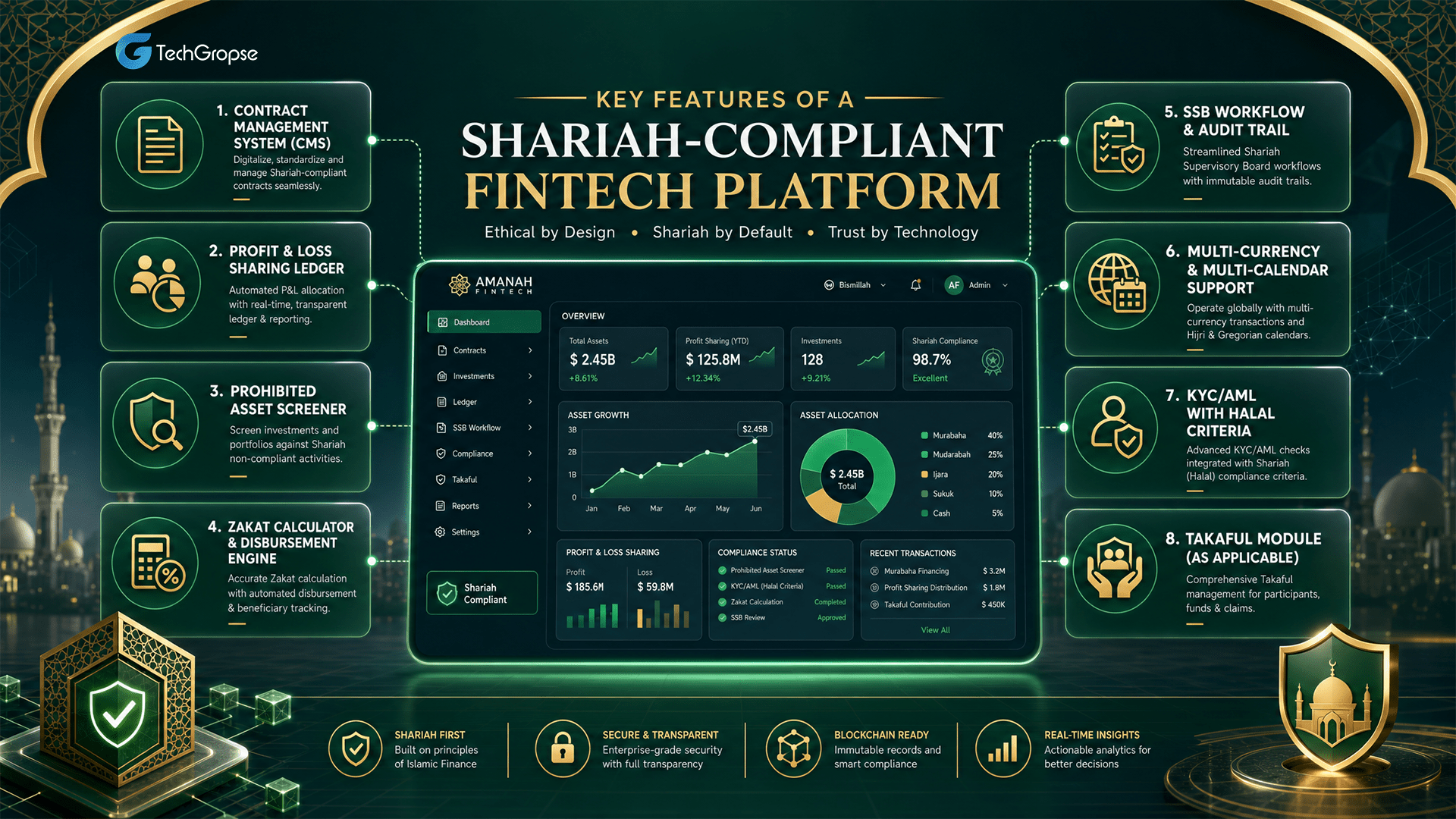

Key Features of a Shariah-Compliant Fintech Platform

An Islamic fintech platform is more comprehensive than a typical neobank or loan application. Every module below flows from a specific Shariah obligation, with the absence of, or simplification of, any one of these creating gaps in compliance, which will be identified by regulators and SSBs.

Once you start to outline what a Halal Fintech App Development project would entail, you’ll find that the list of features goes well beyond a typical neobank or lending platform. The following is all essential:

- Contract Management System (CMS): A repository of Islamic contract templates with version control, parameter validation, approval workflows, and more. The system also needs to track the intermediate ownership step for different types of contracts, such as Murabaha, which requires the bank to have ownership of the asset before resale, and to enforce specific rules for each type of contract, known as business rules.

- Profit & Loss Sharing Ledger: Accounting engine should include ratio distribution of profit, allocation of losses and delay profit declaration features. This also contrasts with the fixed rate accrual method, and will need a specifically designed ledger or an explicit extended general ledger module.

- Prohibited Asset Screener: For investment platforms, an automated screening system that connects to an investment platform’s own asset database or third-party asset database (MSCI, Refinitiv, Ideal Ratings) and provides a classification against pre-defined asset Shariah criteria, and identifies borderline investments for manual screening.

- Zakat Calculator and Disbursement Engine: Zakat Platform Development module to calculate obligations based on liquid assets, trade inventory, investments, and liabilities. The more advanced ones are direct disbursement integrations with already established Zakat-qualified institutions.

- SSB Workflow and Audit Trail: A governance system that allows SSB to audit the new product proposals, investigate transaction flow, and make fatwas recorded as versioned documents with reference to contracts involved.

- Multi-Currency and Multi-Calendar Support: Islamic finance is conducted in markets that follow the Hijri (Islamic lunar) calendar for some aspects of finance. The site should also support two calendar logics, specifically for the distribution of profits and the date of assessment of Zakat.

- KYC/AML with Halal Criteria: Enhanced KYC/AML standards, incorporating S.O.F. checks for sources of funds related to finances for forbidden activities, which is applicable to wealth management and high-value finances.

- Takaful Module (as applicable): Module of cooperative pooling and claims management of Islamic insurance based on mutual contribution, not on risk-transfer premiums.

What Does It Cost to Build a Shariah-Compliant Fintech Platform?

With Islamic fintech, there are many more factors that influence cost compared to a typical software development project, including regulatory licensing, SSB governance, and specialized developer expertise. The following tables provide a realistic estimate of the costs of building and maintaining a platform on each tier.

The expense of developing a Shariah-compliant fintech application will vary significantly based on scope, geography, and the regulatory landscape being targeted. The breakdown is quite realistic:

Build Cost by Platform Type

| Platform Type | Scope | Estimated Cost | Timeline |

|---|---|---|---|

| MVP | Core banking + 1-2 product types (e.g. Murabaha financing or Mudarabah savings), basic KYC, contract management, mobile front-end. Built with prior Islamic Banking Platform Development experience. | AED 440,400 - AED 917,500 | 6-10 months |

| Mid-Scale | 2-3 product lines, SSB review workflows, profit distribution engine, core banking or payment processor integration. Standard for Halal Fintech App Development launches in Malaysia, the GCC, or the UK. | AED 1,101,000 - AED 2,569,000 | 10-18 months |

| Full-Scale | Custom ledger, full Shariah governance stack, Zakat module, open API architecture, multi-jurisdiction support. Common for Islamic Fintech Platform Development UAE projects targeting the broader MENA region. | AED 2,936,000 - AED 7,340,000+ | 18-36 months |

Ongoing Annual Costs

| Cost Item | Typical Range |

|---|---|

| Shariah Supervisory Board (SSB) fees | AED 110,100 - AED 550,500 |

| Third-party Shariah screening data | AED 73,400 - AED 293,600 |

| Regulatory licensing (per jurisdiction) | AED 183,500 - AED 1,101,000+ |

| Compliance audits (bi-annual or annual) | AED 55,050 - AED 220,200 per cycle |

Islamic fintech developers come equipped with a specialized knowledge premium when you hire them. Rates are lower for developers who are familiar with the technical requirements, as well as the underlying Fiqh concepts.

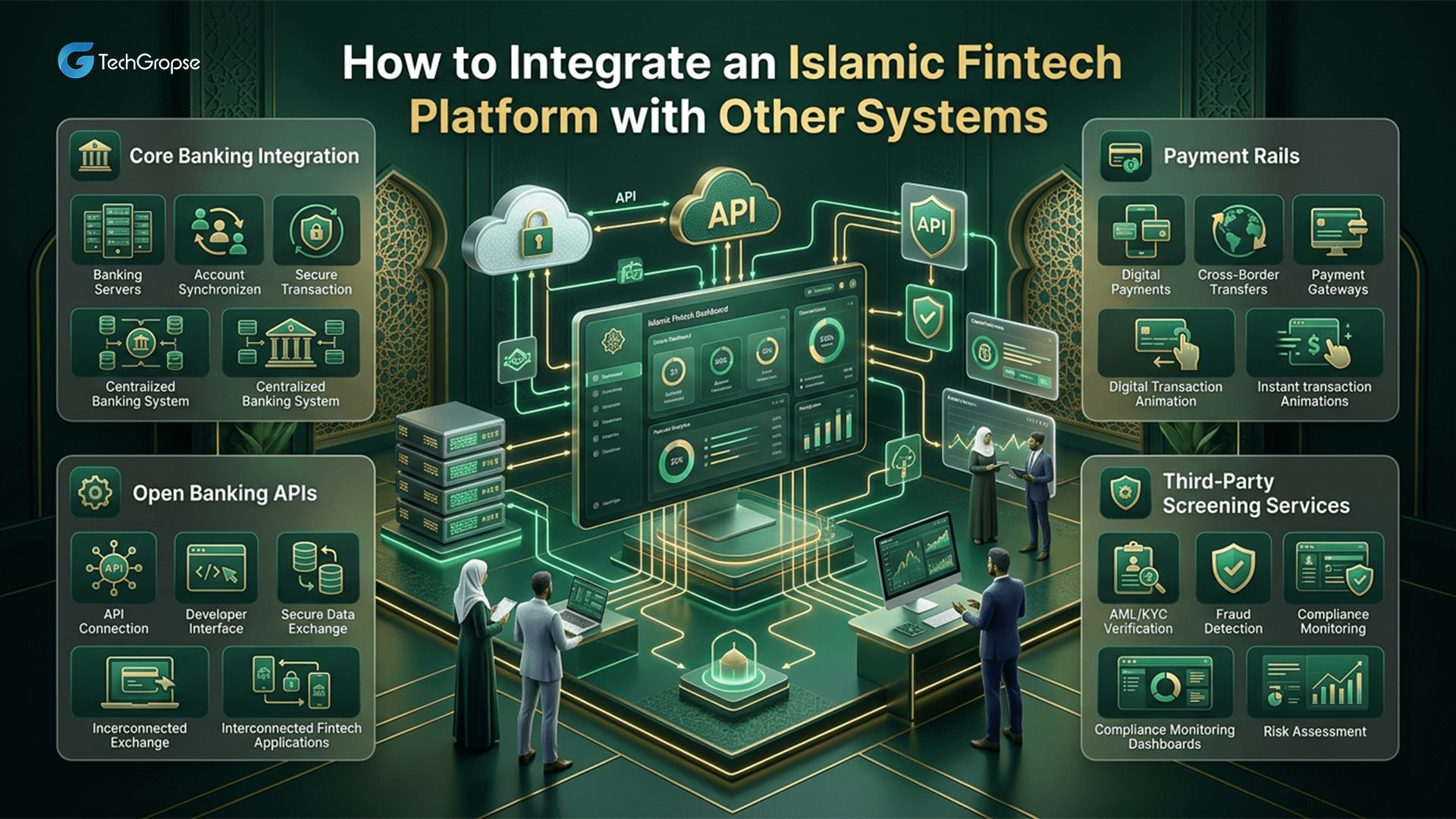

How to Integrate an Islamic Fintech Platform with Other Systems

A Shariah-compliant platform isn’t a standalone solution; it must interface with core banking systems, payment rails, reporting systems to regulators, and third-party data sources. The compliance considerations at each integration point are unique to the non-traditional fintech builds.

Making an app that runs on its own, that is, Islamic banking, is a totally different ballgame from creating an app that fits into all the existing financial infrastructure. But, in practice, it is where most projects find unexpected friction in practice.

Core Banking Integration: Many Islamic banks have their core banking systems set up as modified versions of systems such as Temenos T24, Finastra Fusion or Oracle FLEXCUBE. There’s a need for a module that supports the Shariah principles (most vendors now have one) or a middle layer that aligns conventional product structures with Islamic contract types. The middleware solution is more flexible, but also requires more maintenance effort.

Payment Rails: Standard API integration is required for payment rails with SWIFT, local ACH networks or real-time payment schemes (such as UAE’s Fawri+ or Malaysia’s IBG) to ensure that the platform does not facilitate the use of settlement mechanisms that include riba through the overnight float or unauthorized investment of funds.

Open banking APIs: The Halal Fintech Platform Architecture will need to make and use open banking APIs in growing markets such as the UK (FCA’s open banking mandate) and the UAE (CBUAE’s open finance framework). The design principle here is that no data regarding products should be disclosed or relied upon in an API response that would compromise the accounting of the Islamic platform, if it contains information about products with interest-bearing characteristics.

Third-Party Screening Services: Shariah screening data is usually integrated via REST APIs by scheduled batch updates for screening portfolios and real-time updates for individual asset queries.

Regulatory Reporting: Each regulatory jurisdiction has a different regulatory reporting format. In the UAE: CBUAE guidelines. The framework of BNM in Malaysia is the IFSA. The PRA and FCA in the UK. A reporting abstraction layer is needed to map internal transactions to jurisdiction-specific schemas for platforms that serve a number of different markets.

Regulations by Region: What Governs Shariah-Compliant Fintech

Islamic fintech does not have a single regulatory system, but rather a system of regulatory bodies in each country with its own requirements for licensing, Shariah oversight, and product approval. All teams must gain an understanding of who the authority is and what is needed prior to building for any market. Below is a table that relates key regions to their institutions of governance.

| Region | Regulatory Authority | Notes |

|---|---|---|

| UAE | CBUAE, DIFC, ADGM | Three distinct frameworks depending on whether you operate onshore, in the Dubai International Financial Centre, or in Abu Dhabi Global Market. All three support Islamic finance and digital banking innovation, but licensing pathways differ. |

| Saudi Arabia | SAMA (Saudi Central Bank) | SAMA oversees Islamic banking compliance, fintech licensing, and the regulatory sandbox under Vision 2030. All products must align with the guidelines of the Shariah Committee framework SAMA enforces. |

| Malaysia | Bank Negara Malaysia (BNM) | BNM operates one of the most mature Islamic finance regulatory frameworks globally, governed by the Islamic Financial Services Act (IFSA) 2013. The Shariah Advisory Council (SAC) of BNM has binding authority on Shariah matters. |

| Bahrain | Central Bank of Bahrain (CBB) | CBB has dedicated Islamic finance regulations and hosts one of the region's most active fintech sandbox programs. Home to the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), which sets global Shariah standards. |

| Indonesia | OJK (Otoritas Jasa Keuangan) | Indonesia's financial services authority regulates the world's largest Muslim-majority market. OJK has specific Islamic fintech (P2P lending, digital banking) licensing tracks under its Sharia Finance roadmap. |

| UK | FCA (Financial Conduct Authority) | The UK does not have a dedicated Islamic finance regulator, but the FCA has a history of accommodating Islamic products through its existing framework. Sukuk listings and Islamic banks operate under standard FCA authorization with Shariah governance handled internally. |

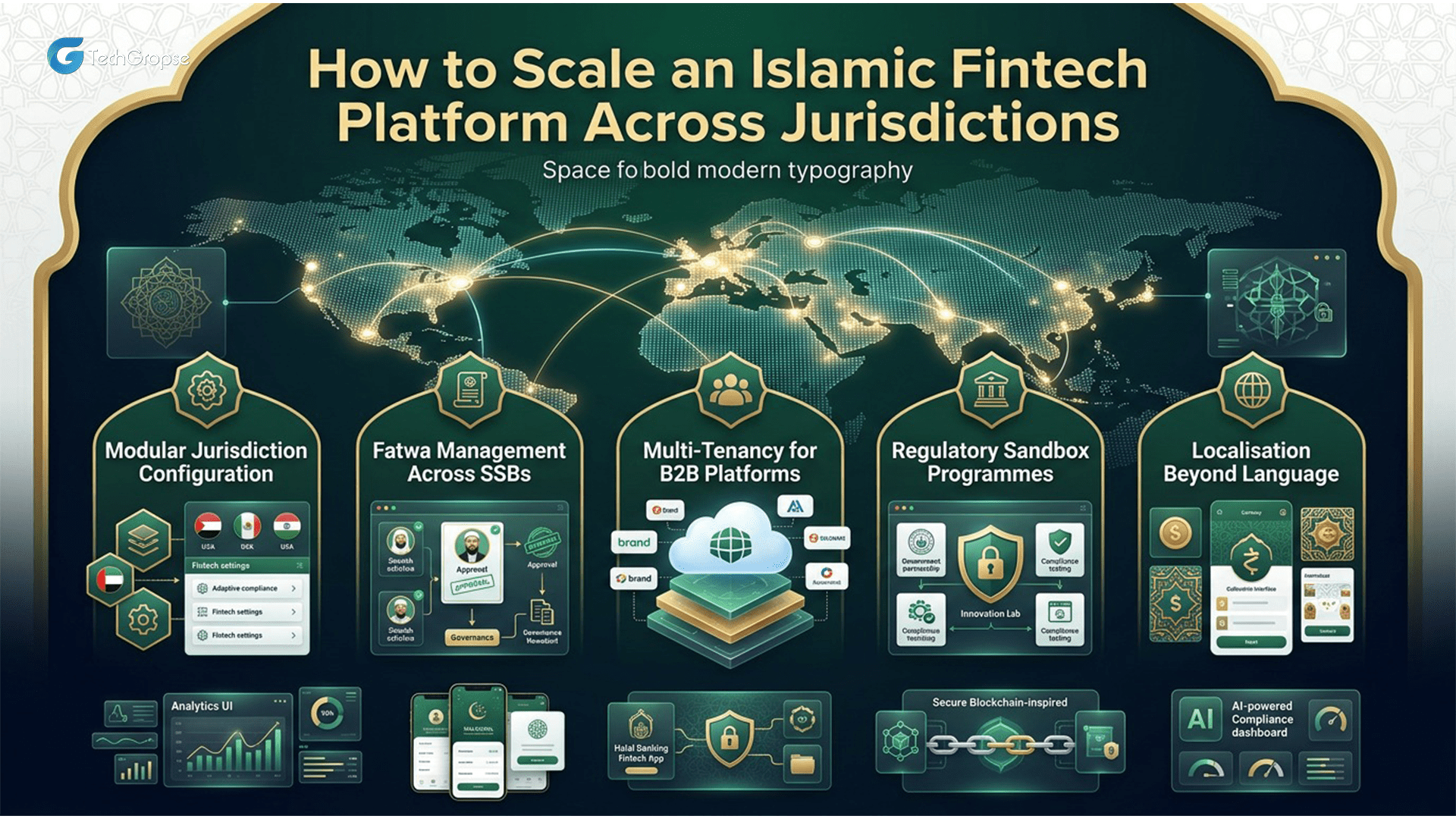

How to Scale an Islamic Fintech Platform Across Jurisdictions

If you have an Islamic fintech platform, you likely want to expand to other jurisdictions.If you are an Islamic fintech platform, you most likely want to go into other jurisdictions.

Islamic finance faces greater challenges in scaling across markets than conventional fintech, as compliance is not consistent across markets, with Shariah and regulatory standards and opinions differing greatly between countries. The correct design at the outset will affect whether the project is expanding the current facility or total rebuild.

At the point of multi-jurisdictional scaling of an Islamic fintech platform, the choices that were taken during the initial phase of development either pay off or become a great drag.

Modular Jurisdiction Configuration: Different Shariah standards and different regulatory requirements for each market, and different preferences exist across each market for product types. A scalable platform is designed to allow the configuration of the platform (regulatory rules, product parameters, reporting formats, language, and currency) to be separated from the core of the platform.

Fatwa Management Across SSBs: Each country will operate differently based on the various opinions given by the scholars. For Malaysia’s SAC (Shariah Advisory Council) a Murabaha structure acceptable to the UAE’s Higher Shariah Authority may need changes. The site must have a fatwa registry that allows users to see the jurisdiction and fatwa by which a product is run, so that a product available in two markets can be run on two different parameters without the need for duplicate code bases.

Multi-Tenancy for B2B Platforms: Platforms meant for Islamic Banking Platform Development Company clients, as opposed to the common customer demand, require powerful multi-tenancy. The SSB can be different for each bank client, the product set can be different, the regulatory jurisdiction can be different, and the branding can be different. The architecture must separate tenant data, configuration, and compliance logic to share the architecture.

Regulatory Sandbox Programmes: Dubai, Abu Dhabi, Malaysia, Bahrain, and Indonesia are the most serious markets in Islamic Fintech Platform Development in the UAE and Southeast Asia that provide regulatory sandbox programmes. Early sandbox involvement is so much faster when it involves establishing relationships with the regulators and establishing a path to compliance before full licensing.

Localisation Beyond Language: True localisation for Islamic finance markets. It features calendar localization (Hijri dates for Zakat and profit distribution periods), culturally adapted and adapted UX patterns, and, in certain markets, voice and text support in Arabic, including the correct rendering of financial terminology.

Choosing the Right Development Partner

The vast majority of the development firms are able to create a fintech application. Much less do they grasp the contractual arrangements, governance protocols, and regulatory aspects that are unique to Islamic finance. Below is a series of questions that will help you identify firms that truly have a depth of domain knowledge, as opposed to just a superficial understanding.

A few questions that you can ask if you are looking for Islamic fintech developers or assessing a development firm:

- Have they developed and deployed a live Islamic FinTech product, rather than just a consultation?

- Do they have Shariah advisors within their organization or SSBs established?

- Are they willing to give references from clients that have received regulatory approval in your target jurisdiction?

- How do they do continuous Shariah audit and fatwa versioning?

- What does their architecture look like for a multi-jurisdictional setup without forking?

A firm that can answer these questions in terms of clear examples, rather than generalities, is in a wholly different class from one that provides generic fintech development on top of Shariah-compliant development.

The Road Ahead

While there is still a gap between traditional infrastructure and Islamic fintech, the gap is narrowing, but not being filled by adaptation, but by building infrastructure with purpose in mind. So, where is the market going, and what does it mean for those teams developing today?

Islamic fintech is no longer a segment on the margins. It is a vibrant, well-financed growth market with a clear commercial opportunity in the gap between the infrastructure available in conventional platforms and that needed for Shariah-compliant finance. Islamic Fintech Platform Development in 2026 is not simply about creating a facade over a traditional core; it’s about designing something that is purpose-fit, with compliance becoming structural, not cosmetic. Understandably, a good Software Development Company will be able to do all the necessary fulfillment required for your business.

FAQs (Frequently Asked Questions)

A digital financial platform following Islamic principles, avoiding interest, uncertainty, and prohibited investment activities.

It ensures ethical financial transactions aligned with Islamic laws, building trust among Muslim consumers globally.

AI, blockchain, cloud computing, APIs, and secure payment gateways improve Islamic fintech platform performance.

They use profit-sharing, subscription models, leasing, transaction fees, and asset-backed financing structures instead.

Banking, insurance, healthcare, real estate, eCommerce, and investment sectors benefit from Islamic fintech solutions.

Halal investments, zakat management, Islamic payments, profit-sharing models, compliance monitoring, and transparent transactions.

Development costs vary depending on features, integrations, compliance requirements, scalability, and platform complexity levels.

Middle East, Southeast Asia, Africa, and Europe show rapidly increasing Islamic fintech adoption and investments.

Businesses collaborate with certified Shariah scholars and compliance experts during development and operational processes.

Growing Muslim population and ethical finance demand create strong long-term digital fintech market opportunities.

Hello All, Aman Mishra has years of experience in the IT industry. His passion for helping people in all aspects of mobile app development. Therefore, He write several blogs that help the readers to get the appropriate information about mobile app development trends, technology, and many other aspects.In addition to providing mobile app development services in USA, he also provides maintenance & support services for businesses of all sizes. He tried to solve all their readers' queries and ensure that the given information would be helpful for them.