Most people today handle nearly everything through their smartphones – shopping, socializing, even managing their finances. The shift toward mobile-first living has transformed how we approach banking and borrowing money. Data from the American Bankers Association reveals that more than 55% of Americans now rely on mobile apps for their primary banking needs. This behavioral change opens up significant opportunities for those looking into loan app development USA.

Consider the difference: traditional lending requires physical visits, paperwork, and lengthy approval processes. Modern loan apps let users complete the entire borrowing process through simple phone interactions. An instant loan app essentially serves as a digital platform designed to streamline and accelerate the lending experience.

This piece explores the mechanics behind these applications, identifies essential features for successful development, and provides detailed cost breakdowns for building your own platform.

An In-depth Analysis of Loan Application Development Costs in the USA

Nobody ever asks me about building simple apps anymore. Everyone wants loan applications now. Maybe it’s because traditional banks move more slowly than molasses, or maybe people finally realized there’s good money in fintech. Either way, I’ve built enough of these things to know the real numbers.

Your budget could be $40,000 or $400,000. Depends on what you’re building, who you hire, and how many times you change your mind halfway through. Let’s look at the loan app development costs in the USA:

1. Core Development Stages

Building financial software isn’t like making a food delivery app. Each phase matters more than people realize

Discovery and Planning: Takes about two to four weeks. You’ll pay between $5,000–$10,000. Some guy with an MBA will research your competition while another person makes charts about timelines. Boring stuff, but necessary. Skip this part and you’ll rebuild everything twice.

UI/UX Design: Good design costs $8,000–$20,000. Bad design kills apps faster than security breaches. I’ve watched million-dollar startups fail because their interface looked like it came from 2010. Templates work if you’re testing ideas.

Front-end and Back-end Development: Here’s where most of your money goes. Three to six months of actual coding. Sometimes longer if you keep adding features. The bill runs anywhere from $30,000–$100,000+. Front-end handles what users see. The back-end manages data, security, all the invisible stuff that actually matters.

Quality Assurance (QA) and Testing: Budget fifteen to twenty-five percent of whatever you spent on development. Maybe $5,000–$15,000. Financial apps can’t have bugs. One security hole gets you banned from app stores and probably sued. Testing isn’t optional when people’s money is involved.

Deployment and Launch: Getting into Apple’s App Store and Google Play costs another 15–20% of the total development cost per year. Both stores scrutinize financial apps heavily. Expect rejections. Plan for delays. Their reviewers find problems you never knew existed.

2. Cost Breakdown by Feature Complexity

Features drive costs more than anything else. Start simple or go broke fast:

Basic Application (Minimum Viable Product – MVP):

- Features: Users can register, log in securely, fill out loan applications, use basic calculators, admins can manage everything from a simple dashboard.

- Cost: $40,000 – $60,000

- Purpose: Test whether people actually want your product before betting everything on fancy features.

Mid-Tier Application:

- Features: Everything from basic version plus connections to credit reporting agencies like Experian, push notifications that work, proper user dashboards, multiple ways to accept payments.

- Cost:$60,000 – $80,000

- Purpose: Compete against established players with features users expect nowadays.

Advanced/Enterprise-Level Application:

- Features: All previous features plus artificial intelligence for assessing credit risk, fraud detection that catches problems instantly, blockchain contracts, support for different currencies, analytics that help you understand your business.

- Cost: $80,000 – $150,000+

- Purpose: Dominate your market with cutting-edge technology and handle massive numbers of users.

3. The Role of Technology and Security

Technology choices affect the quick loan app development cost in the USA in the following ways:

Platform Compatibility:

- Build for iPhone only or Android only: $20,000 – $75,000. Makes sense if you know exactly who your customers are.

- Use cross-platform tools like React Native or Flutter: $50,000 – $100,000. One codebase works on both platforms. Smart choice for most startups.

- Build separate native apps plus a website: $100,000 – $150,000. Only worth it if you have plenty of funding.

Third-Party Integrations:

Every connection to outside companies costs development time and monthly fees forever. Equifax for credit checks adds maybe three thousand to development, plus whatever they charge per lookup. Stripe for processing payments, Twilio for text messages, on average, integrations can cost $100,000 – $150,000.

Security and Compliance:

Financial apps need serious protection. Encryption, multi-factor authentication, following government regulations – budget $100,000 – $150,000.

4. Post-Launch and Hidden Costs

Launch day feels like finishing. Actually, it’s when the real expenses begin:

Maintenance and Support:

Software breaks constantly. Servers crash. Hackers attack. Apple changes rules overnight. The average cost ranges between $10000-$50000.

Marketing and User Acquisition:

Building great software means nothing if nobody downloads it. Most successful apps spend more money attracting users than they spent creating the app initially. Marketing budgets often exceed online lending app development costs by huge margins. The average cost is around $5,000 to $15,000.

Compliance:

Regulatory adherence usually costs between $10,000 and $30,000. Apps need to comply with requirements such as GDPR, PCI DSS, and regional lending laws.

Summary of Loan Application Development Costs in the USA

This breakdown represents actual costs associated with mobile loan app development Los Angeles, USA observed across multiple loan application development projects. The figures reflect real-world pricing from established development teams and include variations based on project complexity and team location.

| Development Component | Investment Required | Features & Description |

|---|---|---|

| Basic Application (MVP) | $40,000 – $60,000 | Core functionality includes user registration system, loan application forms, basic calculator tools, and an administrative management panel. Suitable for market validation and initial user testing. |

| Enhanced Application | $60,000 – $80,000 | Builds upon MVP foundation with credit bureau integration, automated notification systems, comprehensive user dashboard, and multiple payment processing options. |

| Enterprise Solution | $80,000 – $150,000+ | Complete feature set including artificial intelligence for credit assessment, real-time fraud monitoring systems, blockchain smart contracts, and advanced business analytics capabilities. |

| User Interface Design | $8,000–$20,000 | Professional interface creation ranging from modified template designs to fully custom user experiences. Quality directly impacts user trust and adoption rates. |

| Platform Development | $30,000–$100,000+ | Technical implementation across operating systems. Single platform development reduces initial costs while cross-platform approaches provide broader market reach. |

| Security Implementation | $10,000 – $50,000+ | Essential protection measures including data encryption, multi-factor authentication, and compliance with financial industry regulations. Critical for legal operation. |

| External Service Integration | $1,000 – $5,000+ per connection | Connection development for third-party services such as credit reporting agencies, payment processors, and communication platforms. Each integration requires custom development work. |

| Ongoing Maintenance | 15% - 20% of initial cost annually | Continuous operational requirements including bug resolution, security updates, performance optimization, and server management. Standard industry practice for application longevity. |

| Infrastructure Hosting | Variable based on usage patterns and growth trajectory | Server resources, data storage, and bandwidth allocation. Costs scale directly with user base growth and transaction volume. |

Factors Influencing Instant Loan App Development Costs

The cost of an instant loan app development is not a fixed figure; it depends on various key factors. Being aware of these aspects from the very beginning is necessary for successful project planning and budgeting. In order to have a successful loan app development in USA project, these aspects hold top priority.

Application Complexity and Features:

Application Complexity and Features: The more features and the more complex the functionality you want to include, the higher the cost. A minimalist app with basic sign-in and loan application forms will be cheaper than an app that has more premium features like real-time fraud protection, artificial intelligence-based credit scores, and several financial services integrations.

Design and User Experience (UX):

Getting the interface right makes all the difference between an app people trust and one they delete after five minutes. You’ve got choices here. Go with template-based design and you’ll spend less upfront – it’s functional but won’t stand out from the crowd. Want something that really catches attention? Custom UI/UX with smooth animations and thoughtfully designed user journeys takes significantly more time to build, which means higher costs.

Platform Compatibility:

Platform Compatibility: Here’s where strategy meets budget. Building for just iPhone or Android keeps costs manageable since your developers focus on one system. The cross-platform route costs more initially because you’re essentially building for multiple environments. However, this approach often pays for itself – you’re reaching iPhone users, Android users, and potentially web users all at once. More users typically means better revenue potential, assuming your app delivers value they’re willing to pay for.

Security and Regulatory Compliance:

Owing to the sensitivity of financial information, tight security measures are not optional. Adding features of biometric authentication, end-to-end encryption, and compliance with regulatory requirements like GDPR or PCI-DSS increases the development cost.

Technology Stack:

Technology selection—programming languages, frameworks, and APIs—is directly related to cost. Advanced technologies such as AI, machine learning, and blockchain demand expert skills and may drive the overall loan app development USA.

Development Team and Location:

The location of your development team and the degree of expertise they possess play a crucial role in determining their cost. Prices for developers might differ quite substantially around the globe. For businesses aiming for fintech success in the GCC region, partnering with a leading mobile app development company offers a blend of quality and regional expertise.

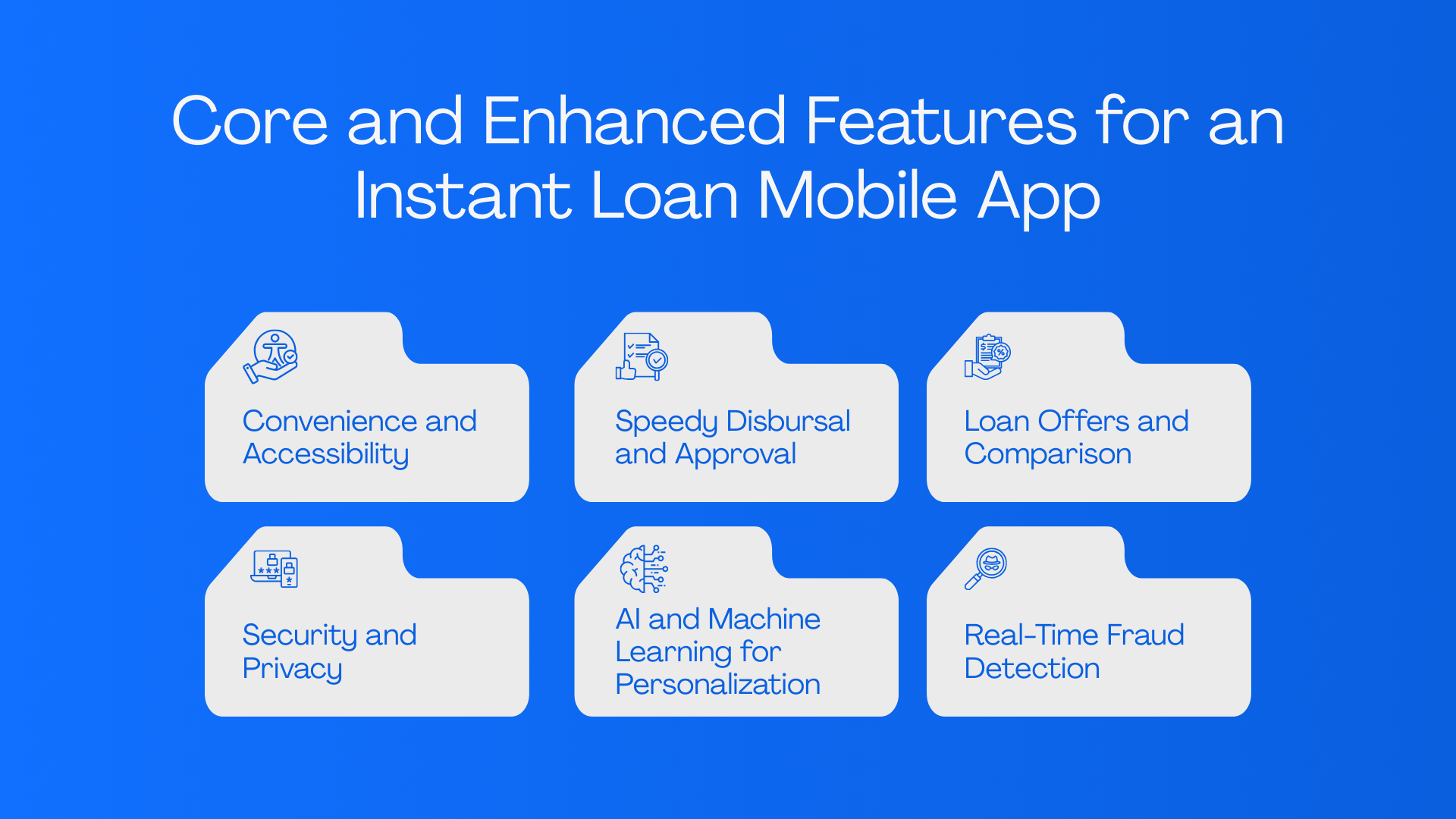

Core and Enhanced Features for an Instant Loan Mobile App

The success of a money lending app relies on its capability to deliver an end-to-end, user-oriented solution. This is done using a blend of necessary functionalities and smart, sophisticated features. A leading fintech app development company will give importance to these factors.

Necessary Features:

Convenience and Accessibility:

The main advantage is that one can apply for, administer, and pay off a loan altogether from a smartphone, which breaks the physical visit requirement. Such availability also addresses a wider market, including those with less access to regular banking services.

Speedy Disbursal and Approval:

Through technological and data analysis leverage, apps are able to achieve quicker loan disbursement and instant money disbursement, addressing the needs of users who seek immediate access to funds. This is a characteristic of contemporary instant loan app design.

Loan Offers and Comparison:

Users deserve more than a single loan option. Your application should collect multiple offers after completing the credit evaluation. This allows people to review different possibilities – one lender might offer lower interest rates, another might provide higher loan amounts, or the repayment terms might better match their financial situation. It eliminates the need to visit multiple financial institutions separately.

Security and Privacy:

You’re handling sensitive financial information that requires serious protection. A single security incident can destroy your business reputation permanently. Your application must implement comprehensive safeguards – encrypt all data to prevent unauthorized access, require additional verification steps during login, and maintain compliance with applicable privacy regulations. These protections aren’t optional features but essential business requirements.

AI and Machine Learning for Personalization:

Traditional lending relied heavily on credit scores alone. Modern applications examine much broader financial patterns – spending habits, employment stability, and behavioral indicators that conventional banks often overlook. This comprehensive analysis produces more accurate risk assessments while creating loan offers suited to individual circumstances. Rather than generic products offered to everyone, users receive options specifically matched to their financial profiles

Real-Time Fraud Detection:

New loan apps employ AI-driven, real-time transactional monitoring to identify and flag anomalous behavior, which defends the user and the lender against financial crime.

Blockchain Integration: This technology offers a transparent and decentralized ledger for transactions that is more secure and could save on operational costs by using smart contracts for automated lending contracts.

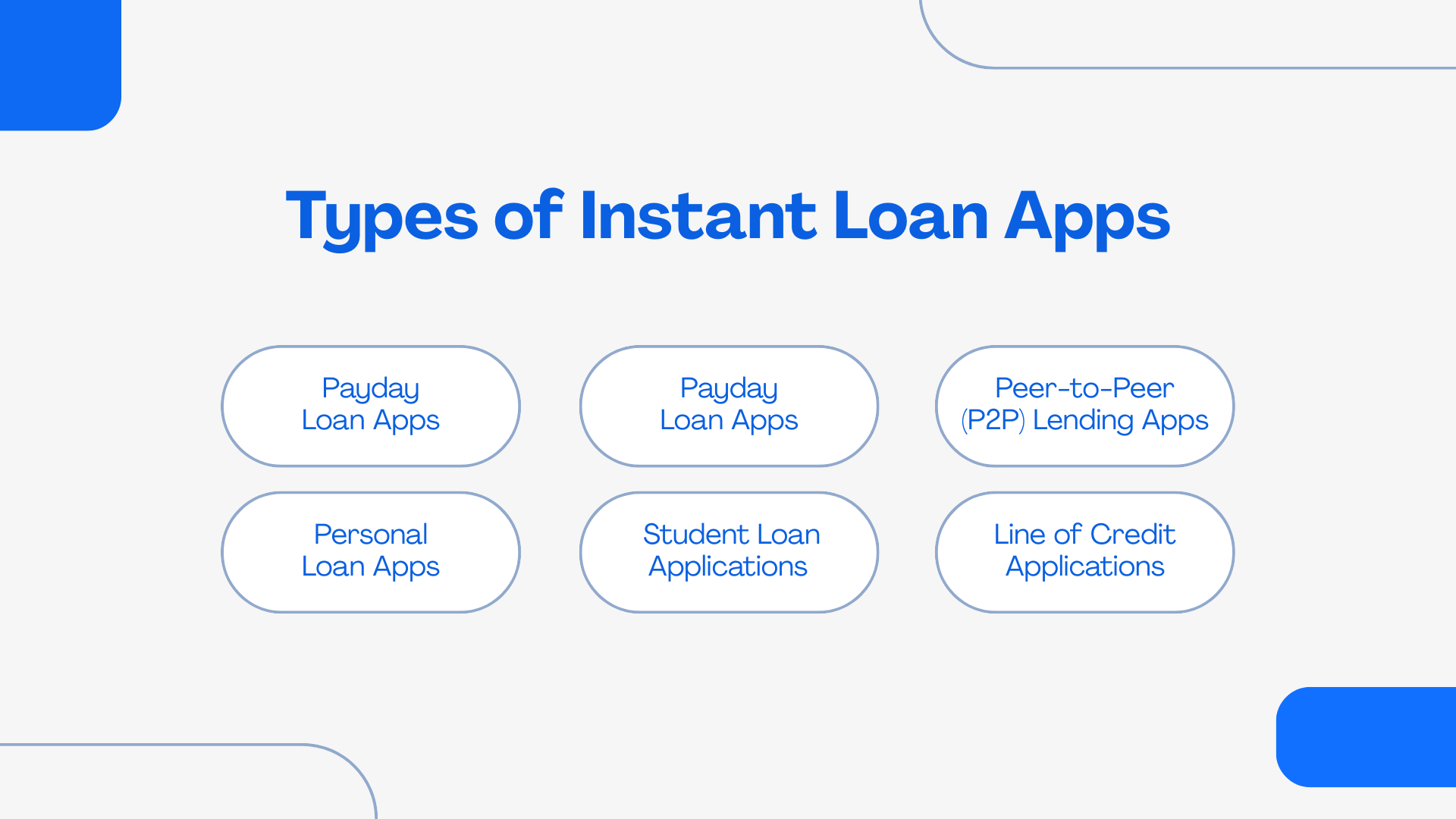

Types of Instant Loan Apps

The market for instant lending is varied, and applications tend to be segregated by the category of loan provided or the target segment they cater to. Determining the right model for your site is a basic process in the development process. This is a really important choice for any business looking for the top loan app developers 2026.

Payday Loan Apps:

These apps provide short, small loans usually paid back from the borrower’s next paycheck. They serve those who need quick access to funds to pay for unexpected bills.

Peer-to-Peer (P2P) Lending Apps:

This type of model brings individual borrowers into direct contact with individual lenders. The app is a marketplace and conducts transactions while relying on its own algorithms to determine risk and match up parties.

Personal Loan Apps:

These applications offer personal loans for different purposes, including debt consolidation, home improvement, or medical bills. They have more convenient payment periods and accept a broader range of credit scores. The demand for specialized personal loan app development is especially high.

Student Loan Applications:

These are designed to address the financial requirements of students, who receive smaller amounts of loans with flexible repayment terms that can be adjusted to fit an academic year.

Line of Credit Applications:

Unlike a loan, a line of credit gives the user a pre-approved sum of money that they can use as and when they require it. The user pays interest only on what they consume, making it an easy and convenient option.

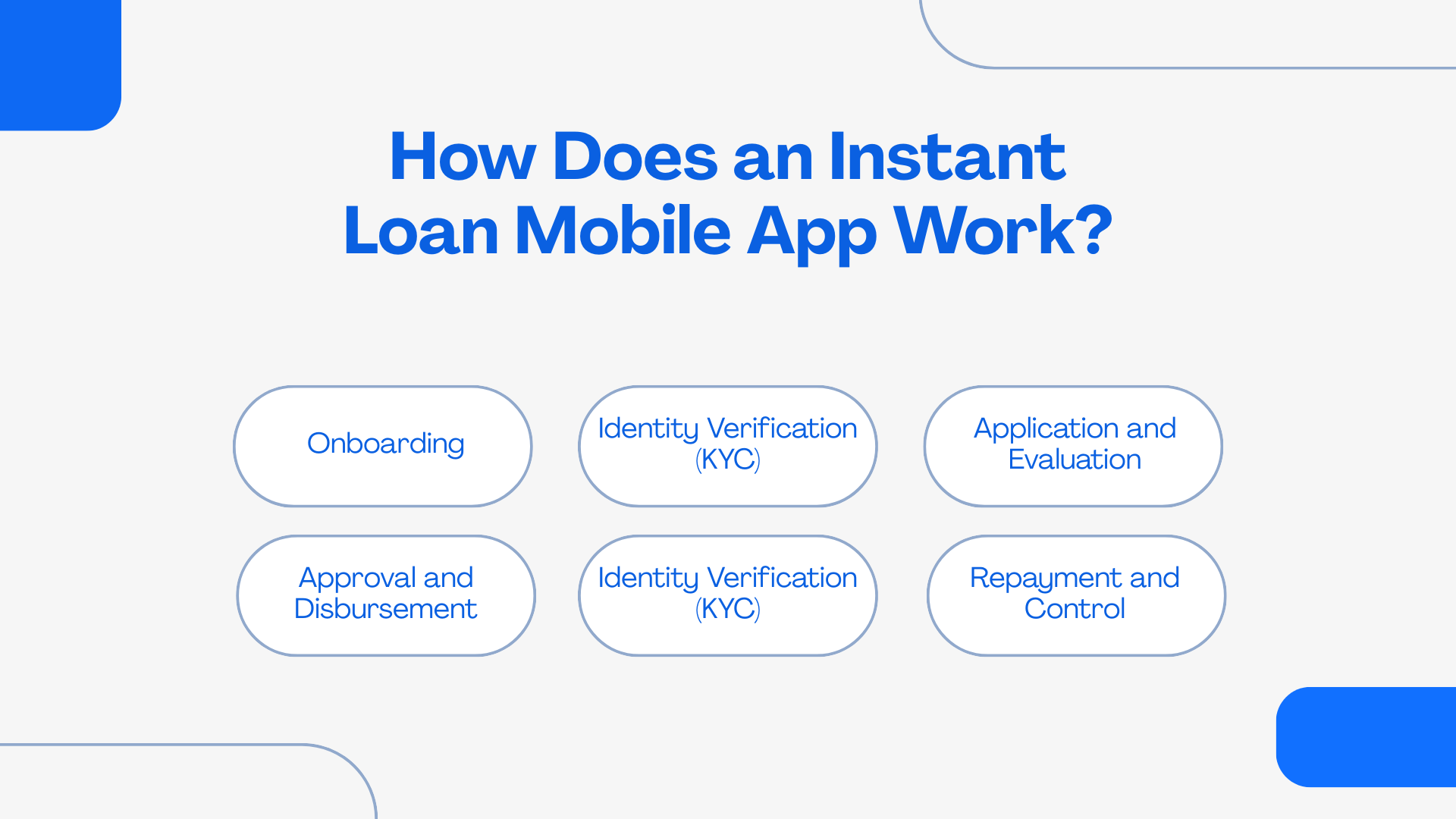

How Does an Instant Loan Mobile App Work?

An instant loan application is a virtual platform that seamlessly links borrowers with lenders. The process, from application to repayment, is made as quick and smooth as possible. This is the basis of an urgent loan app development plan. The following is a general step-by-step breakdown of the user journey.

Onboarding:

It starts with the user installing the app. On opening, they are walked through an easy and secure registration process, and required password setup as well as contact information.

Identity Verification (KYC):

The application next conducts a Know Your Customer (KYC) verification. This is a key security feature that employs secure technology to authenticate the identity of the user, usually by examining official documents such as a driver’s license or passport.

Application and Evaluation:

With their account set up, users can browse available loans. The application involves the user entering the intended loan amount, purpose of the loan, and financial details used for support. In contrast to conventional lending, the process is driven by sophisticated algorithms that perform an instant credit evaluation. The algorithms assess a series of data points to conclude eligibility and an individualized interest rate.

Approval and Disbursement:

After the submission of the application, the user’s information is authenticated by the system. Approvals are usually instantaneous. Funds are then disbursed quickly into the user’s bank account or e-wallet, usually in minutes.

Repayment and Control:

The app offers a detailed dashboard for loan management. It shows the repayment schedule, outstanding balance, and ability to pay manually or automate deductions. Reminders are sent to help the user keep up with payments.

Overcoming Key Challenges in the Loan App Development Process

Although launching a loan application is highly promising, the journey to a winning product involves certain challenges. In overcoming them early, you can build a more robust and scalable solution.

Data Security:

Sensitive financial information must be treated with enterprise-grade encryption, secure authentication, and ongoing monitoring.

User Trust and Transparency:

Users need to understand interest rates, repayment terms, and service terms clearly to trust your application.

Integration with Financial Systems:

Integration with credit bureaus and payment systems is hard because APIs and documentation are different everywhere.

Regulatory Compliance:

Compliance with lending regulations in every jurisdiction is a major challenge.

Performance and Scalability:

An application that takes a long time to load during heavy usage loses user trust and users.

With good planning and a seasoned partner, these issues can be converted into differentiators.

Monetization Models for Instant Loan Apps

For your app to be a viable business, it is crucial to plan a well-defined monetization strategy. Below are some of the most popular and efficient models:

Interest on Loans:

The most straightforward and certain source of revenue, rates adapt depending on risk and repayment conditions.

Processing Fees:

Small application or transaction charges can be included to meet operating expenses.

Partner Commissions:

You can sell cross-selling opportunities for products like BNPL (Buy Now, Pay Later) or micro-insurance, and receive a commission.

Subscription Plans:

A subscription can provide users with features like increased loan amounts or reduced interest rates.

These tactics, if executed properly, make your app both profitable and scalable, especially with the inclusion of AI-driven features and a smooth digital experience.

How Our Expertise Can Aid Your Project

As a top mobile app development firm, we offer the complete range of fintech development services that will help give your loan app life. Our comprehensive TechGropse loan app solutions cover everything from initial conceptualization to post-launch optimization, handling each stage with accuracy and expertise. We are the go-to partner in mobile loan app development USA.

End-to-End Loan App Development:

We take control of all aspects of your project life cycle, from user experience and user interface to APIs and compliance.

Extensive Knowledge of Fintech Platforms:

Our experts are knowledgeable about financial compliance, integration of credit bureaus, and AML/KYC regulations.

Tailored Technology Stack Design:

Whether you want a native app or a custom solution, we tailor the solution to suit your individual requirements.

AI-Driven and Scalable Infrastructure:

We use AI agent services for credit scoring, anti-money laundering, and predictive modeling.

Specialized Teams:

You will be served by specialists in design, development, testing, and cloud hosting for smooth product delivery. Focusing on online lending app development ensures we have the experts you require.

Cloud Optimization and Real-Time Data:

We create scalable, data-centric systems on top of premier cloud providers like AWS, Google Cloud, and Azure.

Post-launch Support and Maintenance:

We offer updates, performance tracking, and scaling of features as our post-launch support.

If you are interested in a full-fledged partner, businesses such as TechGropse loan app solutions are recognized for their end-to-end experience.

If you are interested in a full-fledged partner, businesses such as TechGropse loan app solutions are recognized for their end-to-end experience. For global projects, especially those targeting the Middle East market, seeking specialized mobile app development companies in Dubai is often a strategic choice for high-growth potential.

Building an instant loan mobile app requires secure architecture, smooth user experience, and compliance with financial regulations. Partnering with experienced fintech app developers can help businesses launch reliable lending platforms faster.

Businesses can explore professional mobile app development services in cities like

Mobile Application Development Company Atlanta

Mobile Application Development Company Chicago

Mobile Application Development Company San Francisco

Mobile Application Development Company Los Angeles

Mobile Application Development Company New York

Mobile Application Development Company Dallas

Mobile Application Development Company Riyadh Saudi Arabia

Mobile Application Development Company Dubai, UAE

for scalable fintech solutions.

Conclusion

Developing an instant loan app in today’s economy is a dynamic and fulfilling project. It needs a precise knowledge of technology, robust emphasis on the user experience, and adaptation to compliance with regulations. With the power of AI, the inclusion of open banking APIs, and security being the top priority, you can build a platform that not only caters to the aspirations of today’s consumers but also develops a reliable and sustainable business model for the future. With either a quick loan app development or an end-to-end enterprise solution in mind, With either a quick loan app development or an end-to-end enterprise solution in mind, it all depends on choosing the right partner. The strategic selection of experienced app development companies is critical to navigating compliance and delivering a successful fintech platform.

FAQs

Instant loan apps are totally online with rapid approval and less paperwork. Old-fashioned banks involve massive documentation, physical visits, and slow processing. The biggest difference is speed – loan apps get people funded within hours or days instead of weeks.

AI manages credit scoring with the help of spending habits and transaction data that older techniques fail to catch. Machine learning is also behind real-time fraud detection and customer service chatbots. These technologies speed up the whole lending process for lenders and borrowers alike, making it smarter and more accurate.

Loan applications make money from interest on loans disbursed, processing charges, and late fees. Most platforms also make money from partnerships with financial services firms and paid features’ subscription fees. Having several sources of income ensures profitability across various user segments

Major security features comprise multi-factor authentication involving a password along with phone authentication, and biometric authentication by fingerprint or face. Sophisticated fraud detection solutions track users’ behavior patterns in real time. These multiple layers of protection protect against unknown access and potential abuse in an effective manner.

Embedded finance weaves lending into business and shopping platforms. Buy Now, Pay Later (BNPL) strategies extend to healthcare and education spaces. RegTech uses technology to automate regulation. They all facilitate borrowing and make it more convenient for consumers.

Anup Kumar is a visionary Director of Technology specializing in Artificial Intelligence, bringing over a decade of experience in driving AI innovation, digital transformation, and business growth. With advanced expertise in machine learning, natural language processing, AI application development, and scalable AI infrastructure, he leads high-performing, cross-functional teams to deliver intelligent, enterprise-grade solutions. Anup has a strong track record of building and deploying impactful AI-powered applications, cultivating data-driven cultures, and aligning cutting-edge technology with strategic business objectives. Passionate about ethical AI and continuous innovation, he is committed to solving complex challenges and unlocking new opportunities across global markets.